Summary

The final quarter of 2025 capped a year defined by remarkable economic and market resilience amidst significant policy uncertainty. The underlying macroeconomic data was surprisingly positive in the face of tariff volatility, multiple geopolitical conflicts, a government shutdown, and bubbling fears around Federal Reserve independence. GDP growth averaged 2.5% through the first three quarters, unemployment remained a percentage point below the 75-year average rate of 5.7%, consumer spending was robust, and inflation remained below 3.0%. This environment supported a third consecutive year of above-average equity market returns and robust performance for fixed income assets as the Fed began monetary easing. As we look toward 2026, Guyasuta remains focused on navigating turbulent markets with the same disciplined and data dependent approach to risk management that has successfully served our clients for over four decades.

The Economy

Traditional macroeconomic indicators became increasingly difficult to interpret in the fourth quarter, as a record long 43- day government shutdown led to delayed and withdrawn economic data releases. The data disruption and shifting trade policy forced investors to seek alternative data sources and rely on public company reports to piece together the economic puzzle. As the quarter progressed, the fundamental pillars of a healthy economy emerged. GDP growth continued its rebound from Q1 lows, posting 3.8% and 4.3% growth in Q2 and Q3, respectively, and expectations for Q4 growth are ~3.0%. Consumer spending, which historically drives the lion’s share of domestic growth, remained healthy with retail sales rising 4.1% year-to-date, despite persistent inflation between 2.3% and 2.8% throughout the year. Wage growth consistently outpaced inflation, creating real purchasing power, and consumer balance sheets are the least leveraged since the 1990’s with credit card delinquency rates of ~3.0%, lower than any period in the last two pre- pandemic economic cycles. While the labor market continues to cool, with nearly no job growth over the last four months and unemployment rising from 4.3% to 4.6%, initial jobless claims have not risen. This data combined with shocks like DOGE job cuts, AI-driven productivity gains, and new immigration policies, present a labor market in flux rather than one on the brink of collapse. Altogether, the American consumer and economy appear to be on solid footing despite the headlines. We will be cautiously watching the incoming data over the coming months.

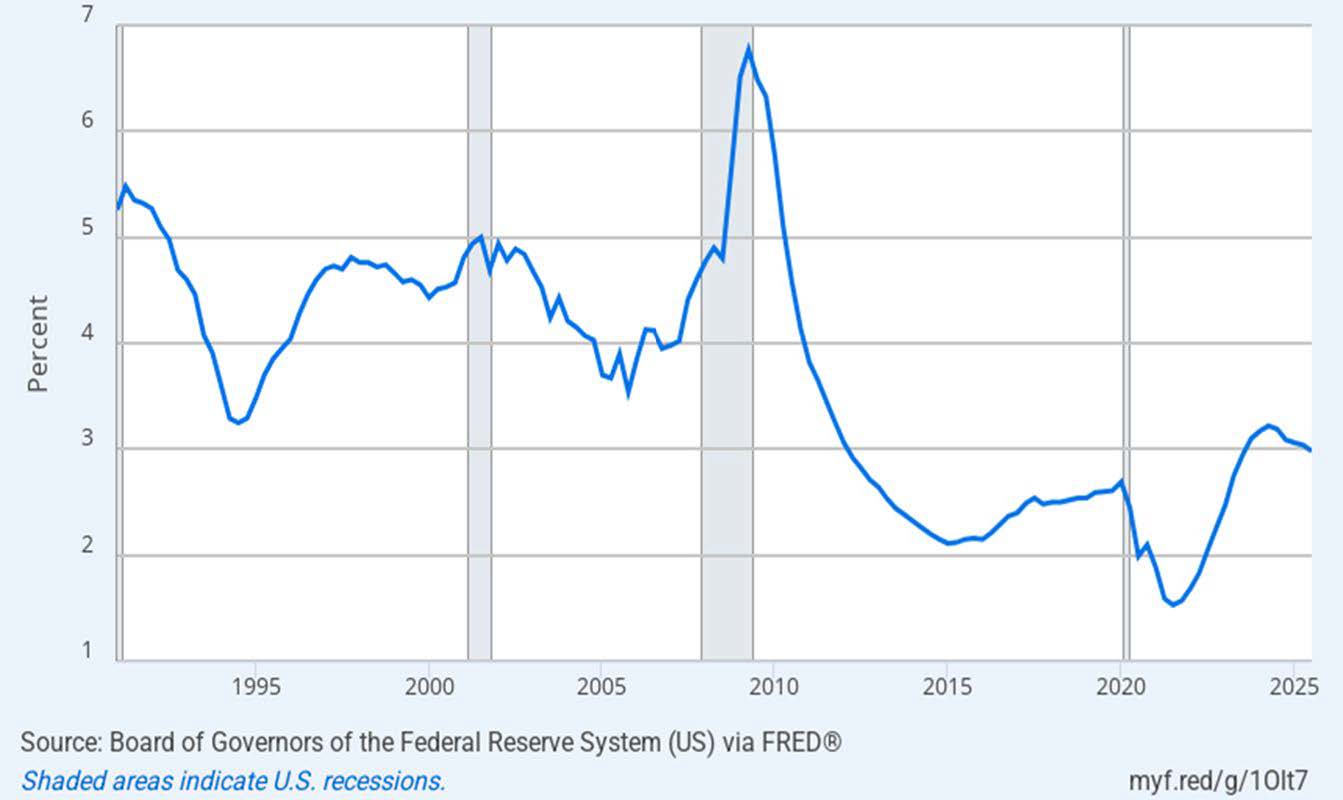

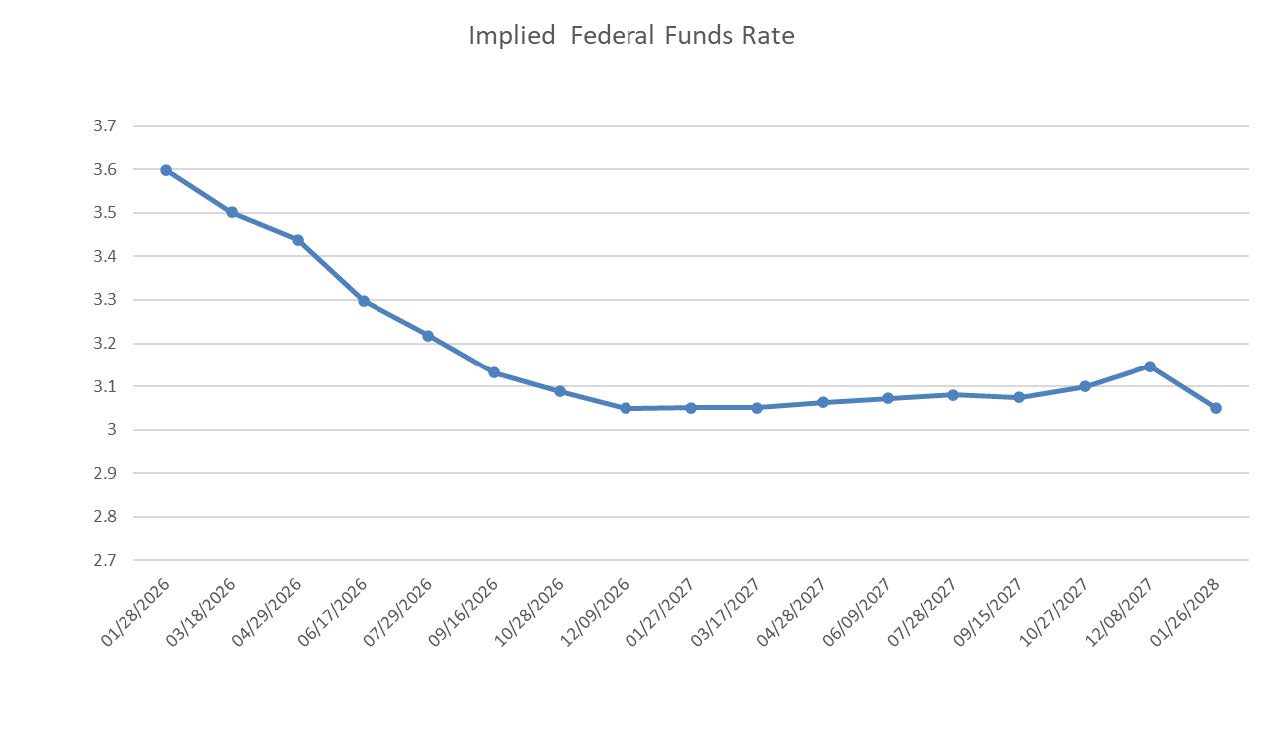

The Federal Reserve continued monetary easing in the quarter, delivering two more 25 basis point (bps) rate cuts, bringing the benchmark rate range to 3.50% – 3.75%. These reductions reflected the central bank’s recognition of a softening labor market and the absence of the inflation pressure that many feared would follow the April tariff announcements. The Federal Reserve’s December “dot plot”, which depicts individual board members’ views on future interest rates, suggests only one rate cut in 2026, whereas financial markets are pricing in two additional cuts, creating a divergence in expectations. Importantly, a new Federal Reserve Board Chairperson will be appointed in May, which has kindled fears that the Fed’s independence will be at risk if the new Chairperson follows the President’s goal of lower rates. This is a known unknown, and the fear is that if the Fed does dramatically reduce the Federal Funds Rate (short- term rate), long-term rates may rise as the perceived risk premium would increase due to a lack of trust in the rate setting policy. We will monitor this as the process unfolds.

Unexpected growth in GDP, real wages, and consumer spending demonstrated the resilience of the economy in 2025, powering performance in financial markets. While there are potential concerns, including AI investment’s substantial contribution to GDP growth (estimated at over 1% of overall growth), labor market stability, a potentially delayed impact of tariff-induced inflation, and Fed independence, we are cautiously optimistic that true economic conditions are being distorted by policy-driven shocks and the government shutdown. As these shocks normalize, we think a strong economy will emerge. We remain vigilant in monitoring these trends and will adjust our strategy accordingly as the facts present themselves.

Equity Markets

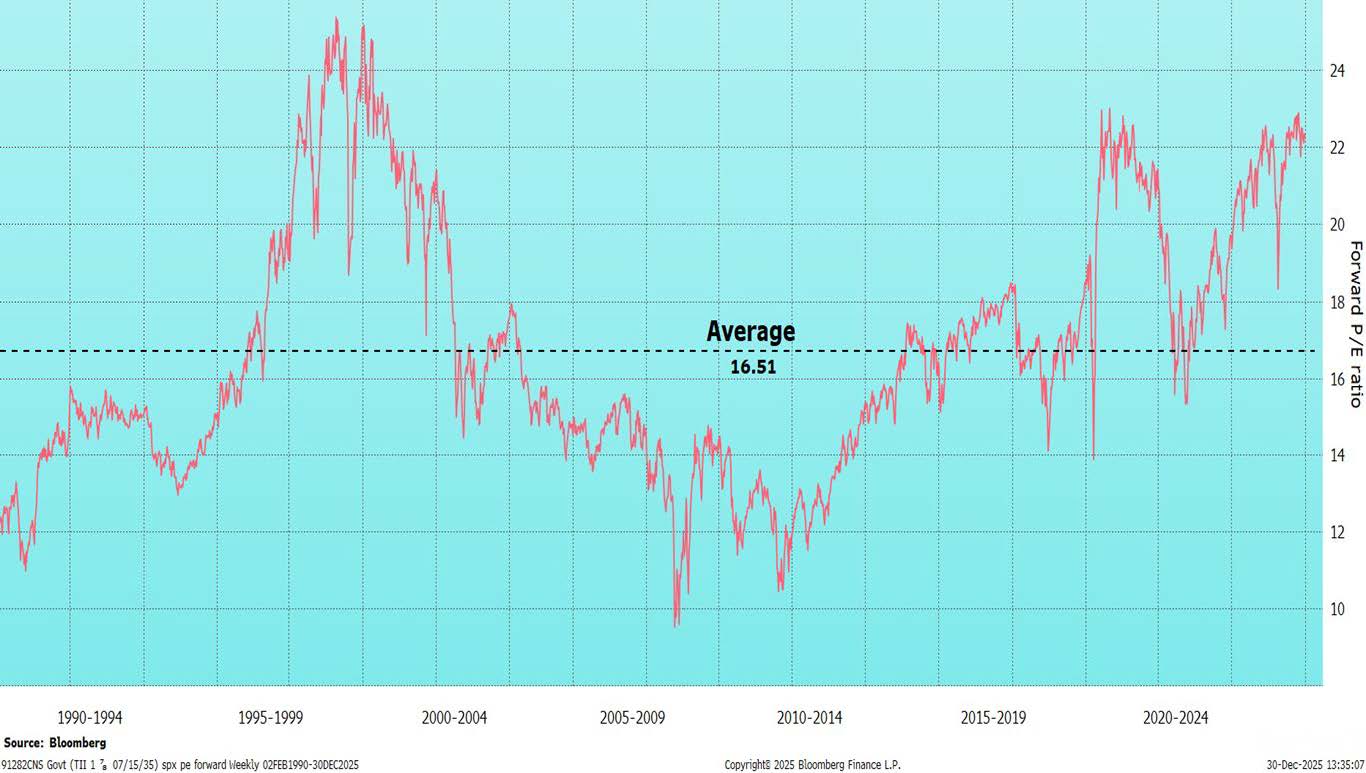

U.S. equity markets concluded 2025 with another year of exceptional performance, marking the third consecutive period of above-average returns for the major indices. The S&P 500 and NASDAQ gained 17.9% and 21.1%, respectively, the equal-weighted S&P 500 rose 11.4%, and the DOW increased 14.9%. This achievement is particularly notable given the extreme volatility witnessed in April, when the tariff announcement triggered a swift 10% to 20% correction across these indices. The market’s ability to recover so rapidly once those policies were paused highlighted the underlying strength of corporate earnings growth, investor confidence, and resilient secular growth themes like AI. While the S&P 500 remains near record highs with a full valuation (22.3x forward earnings), the equal-weighted index showed improved relative strength in December. We believe this emerging expansion of market breadth is positive for the long-term health of the current bull market cycle.

A significant shift occurred during the fourth quarter as investors moved away from the extreme concentration in the “Magnificent Seven” that characterized the first half of the year. Healthcare emerged as a standout performer, gaining 11.3% in the fourth quarter as investors sought out defensive growth at more reasonable valuations. In contrast, artificial intelligence leaders like Nvidia, Broadcom, and Oracle experienced meaningful drawdowns of -17.4%, -21.0%, and -43.0%, respectively, during the quarter. This was not necessarily a rejection of the AI theme, but rather a rationalization of valuations as the market began to demand clearer evidence of sustainable growth, near-term monetization, and returns on investment. Capital rotated into companies like Alphabet, which demonstrated these qualities with rising margins. This healthy “speculative flush” also extended to other “frothy” areas like cryptocurrencies (Bitcoin -32.3%) and nuclear power stocks (NuScale Power -73.6%).

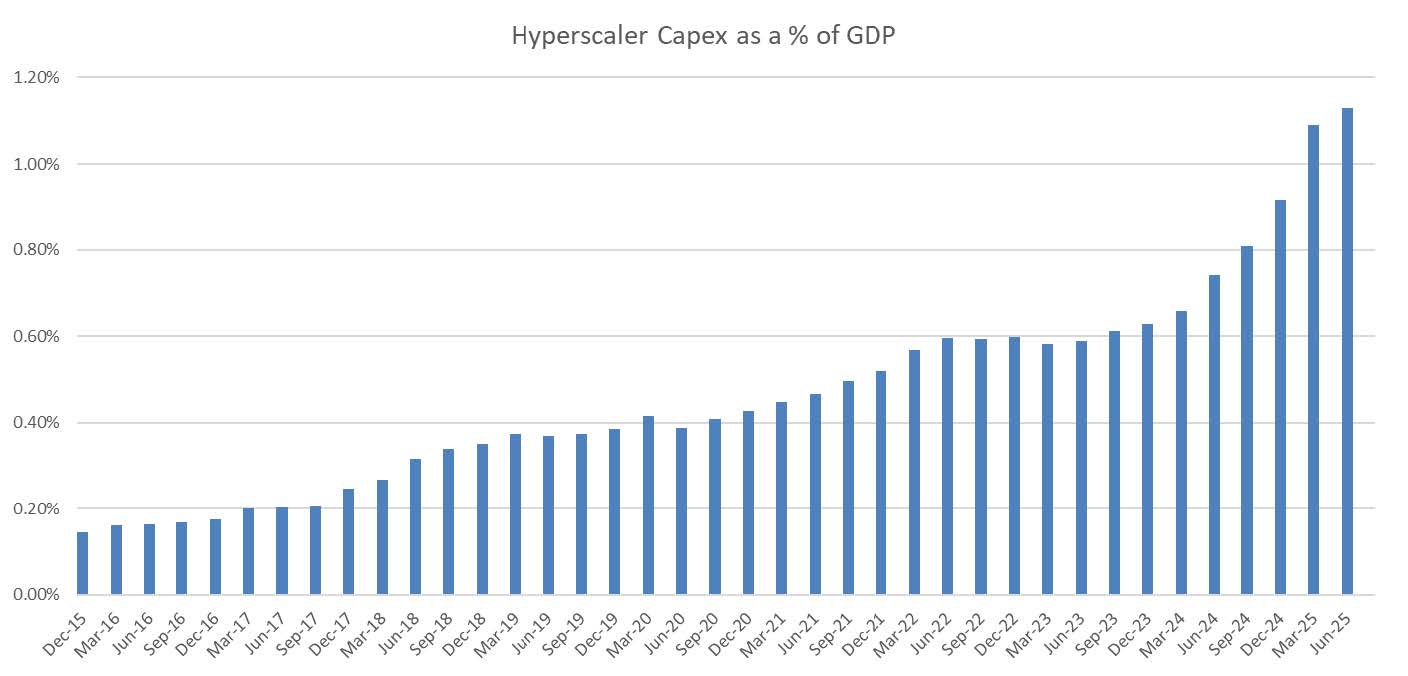

The ongoing debate regarding an AI bubble remains a central theme, as capital expenditure growth rates on data centers continue to defy market expectations and increasingly contribute to economic growth. While there are similarities to the 2000 Dot-com bubble, such as concerns of circular financing deals and growing levels of debt, there are key differences. At the height of the 2000 bubble, leaders like Cisco traded at over 100x earnings, whereas the current leader, Nvidia, trades at 25.6x with free cash flow expected to double over the next two years. Today’s AI leaders are also significantly more profitable accompanied by strong balance sheets compared to the start-ups and over-levered infrastructure companies that characterized the Dot-com era. We have used market volatility to fine-tune our exposure, favoring companies with recurring revenue and the ability to maintain margins in a potentially inflationary environment.

Despite the strong year, we are closely monitoring risks that could challenge equity valuations in 2026. A stagnant housing market, setbacks to the AI theme, and the potential for rising unemployment to finally sap consumer spending are top of mind. Additionally, the valuation gap between the market-capitalization weighted and equal-weighted S&P 500 remains historically wide (22.2x vs 16.9x earnings), leaving little room for error if earnings growth amongst the largest companies were to falter. We are also watching the impact of higher long-term interest rates on corporate borrowing costs, which could eventually weigh on net margins for more leveraged firms. Guyasuta continues to employ a diversified portfolio focused on high-quality companies with durable cash flows and competitive moats capable of navigating market crosscurrents. By focusing on fundamentally strong businesses at reasonable valuations, we believe our portfolio is well positioned to capture upside while being better protected from significant drawdowns.

Fixed Income Markets

Fixed income markets delivered strong positive returns in 2025 with the S&P U.S. Aggregate Bond Index up 7.1% as the Federal Reserve’s transition to a lower rate environment provided a tailwind for bondholders. The yield curve steepened toward a more traditional, upward-slope, as shorter-term two-year yields fell 90 bps to 3.47%, while longer- term ten-year yields compressed only 63 bps to 4.16%. Credit spreads remained remarkably tight throughout the fourth quarter, reflecting a broad consensus among investors that corporate default risks are low. At Guyasuta, our approach to fixed income continues to emphasize high-quality, laddered portfolios customized to the specific liquidity needs and tax situations of our clients. We avoid the temptation to chase yield in lower-quality segments of the market, preferring instead to use fixed income as a reliable anchor of stability within a total wealth framework. This disciplined methodology has allowed our clients to benefit from rising prices due to Federal Reserve rate cuts while maintaining a steady stream of predictable income.

A specific area of emerging risk we are watching is the rapid expansion of lending related to artificial intelligence infrastructure. What began as internally funded cash flow spending by “Big Tech” has expanded into a large wave of debt issuance by a wider range of participants, some of whom carry significant leverage (such as Oracle and CoreWeave, 4.2x and 7.6x net debt/EBITDA, respectively). We are observing a trend where private credit funds and high-yield issuers are taking on substantial debt to fund AI projects with uncertain long-term payback periods. While the level of AI lending is only estimated to be ~2% of the total market, if its growth continues, lenders could become increasingly aggressive and loosen covenants, which could lead to a credit bubble. We are monitoring this activity closely and are encouraged by recent deals that have been canceled due to issuer credit quality concerns. Furthermore, we remain concerned about the independence of the Federal Reserve and how future leadership will manage the tension between fiscal deficits and monetary stability. Our focus remains on owning high-quality credits that can withstand potential shifts in the interest rate path or broader credit market volatility.

Conclusion

2025 demonstrated the market’s resilience in the face of significant disruption. The economy remained strong despite data distortions, equity markets generated a third consecutive year of exceptional gains, and fixed income markets rallied led by the dovish pivot by the Federal Reserve. We continue to monitor the confluence of ongoing risks and look for opportunities with asymmetric risk/return profiles. Guyasuta’s commitment to a disciplined, diversified, and quality- focused investment philosophy remains the cornerstone of our strategy. We are dedicated to ensuring client portfolios are aligned with long-term financial goals and stand ready to adjust as the 2026 landscape unfolds. Thank you for your continued trust and partnership as we navigate these complex markets together, and we welcome any questions.

S&P 500 forward P/E: Market is expensive relative to historical average

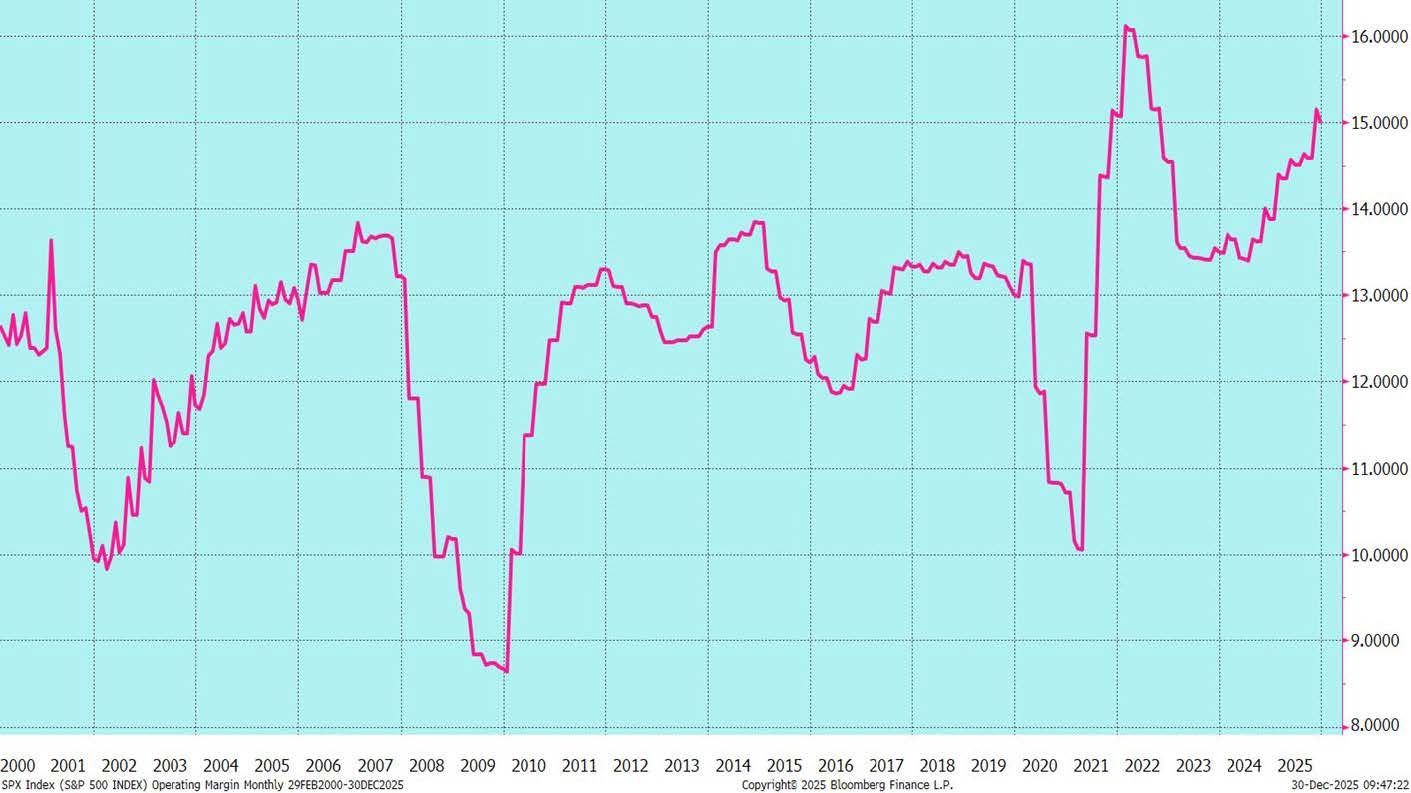

S&P 500 operating margins remain strong despite tariffs and inflation

Artificial Intelligence capital expenditures driving GDP growth

U.S. wage growth is outpacing inflation, a positive signal for consumer spending

Credit card delinquency rate: Not flashing Red

Corporate balance sheets are strong

Fed Funds implied rate & number of hikes / cuts

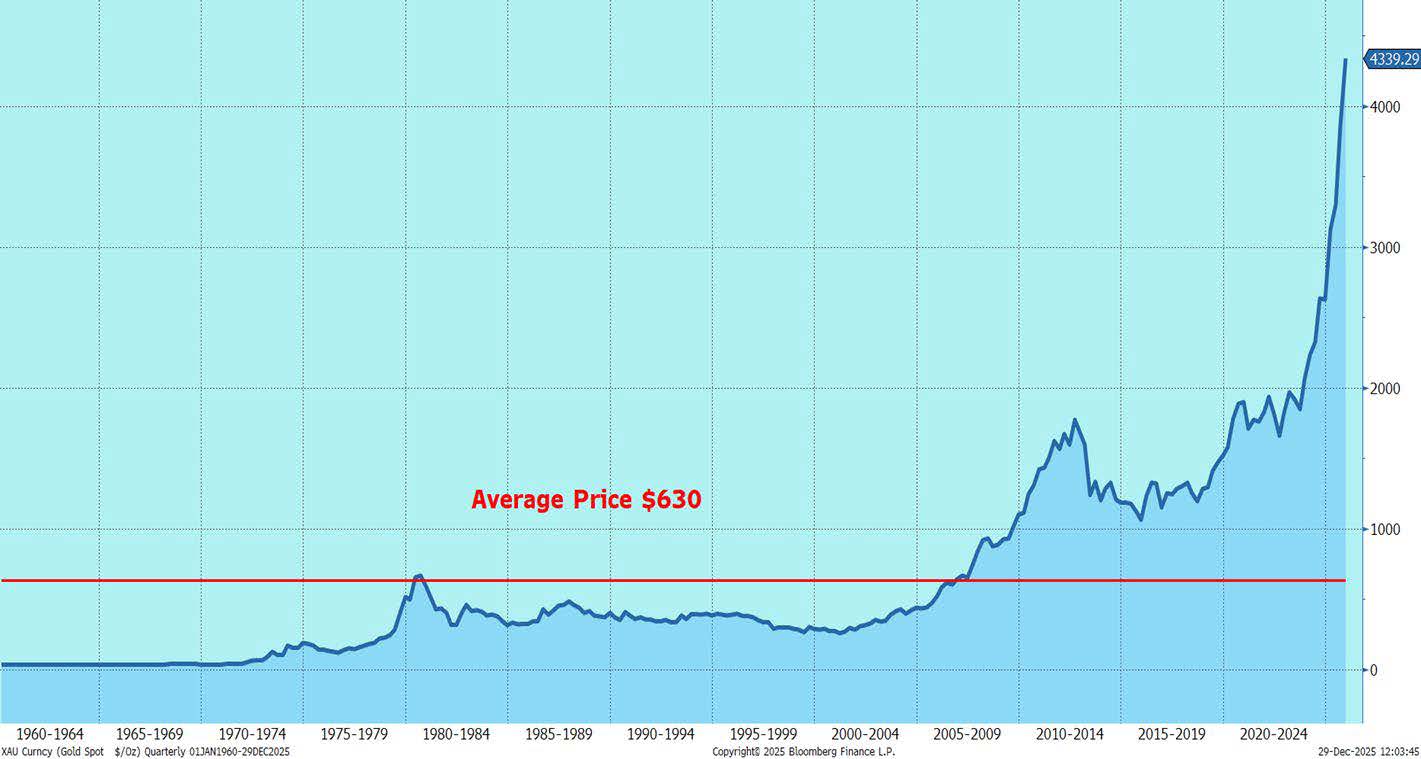

Gold has benefitted from currency risks, inflation and global instability