Summary

The second quarter of 2026 provided a steady stream of disruption and uncertainty in global markets. An escalating conflict in the Middle East led to the closure of the Strait of Hormuz, triggering supply chain bottlenecks and renewed inflation anxieties. These price pressures directly collided with a leadership change at the Federal Reserve, reviving long-standing debates surrounding central bank independence and the future path of interest rates. Despite these events, domestic equity markets showed incredible resilience, climbing to new all-time highs on the back of exceptional corporate earnings. Conversely, fixed income markets experienced elevated volatility as yields surged in response to shifting monetary policy expectations. In this edition of the Market Comments, we will examine the economic impact of geopolitical shocks, the equity market’s performance, and the shifting fixed income landscape.

The Economy

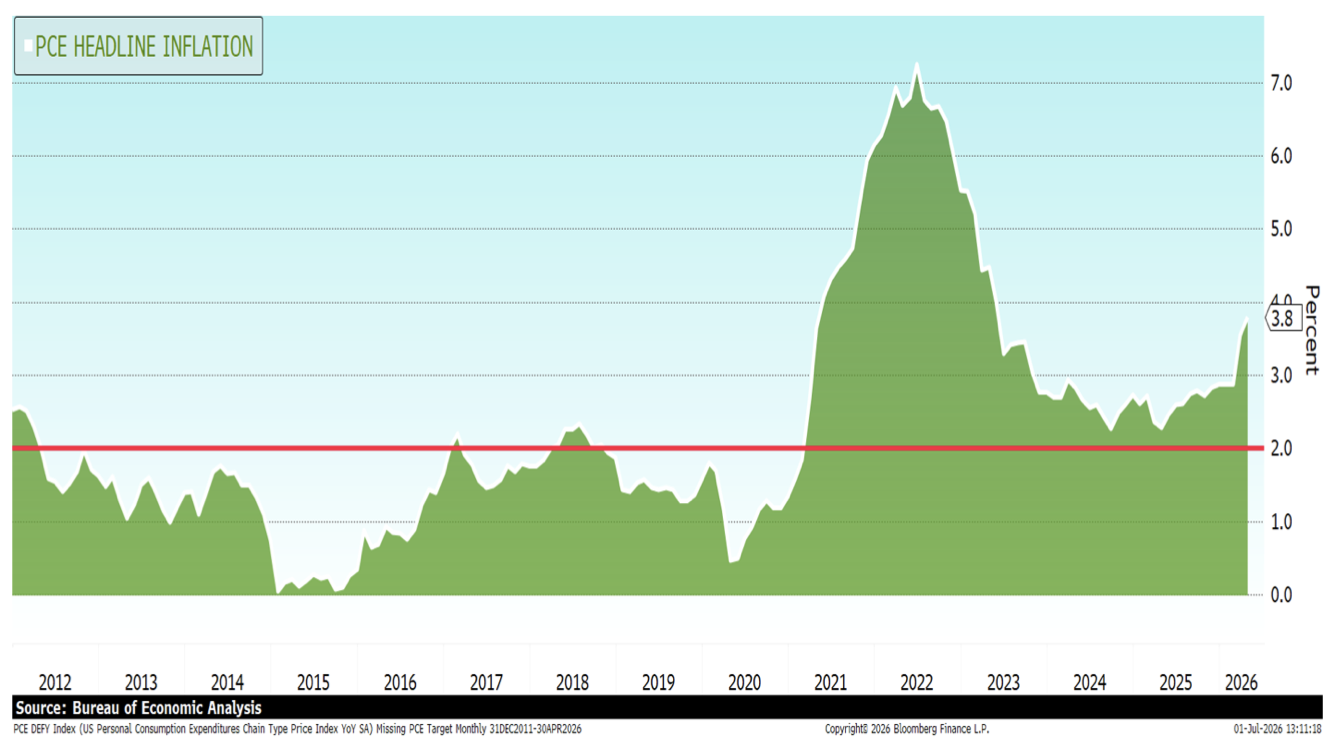

The primary catalyst behind this quarter’s economic shifts was the ongoing conflict in the Middle East, which deeply disrupted international shipping lanes. The prolonged closure of the Strait of Hormuz functioned as a sudden supply chain shock, forcing ships to take longer, costlier transoceanic routes. This logistical bottleneck quickly fed through to consumer pocketbooks, driving U.S. PCE inflation to 4.1% in May. Even after stripping out energy and food prices, core PCE inflation remained stubbornly above the Fed’s official 2% target (3.4% in May).

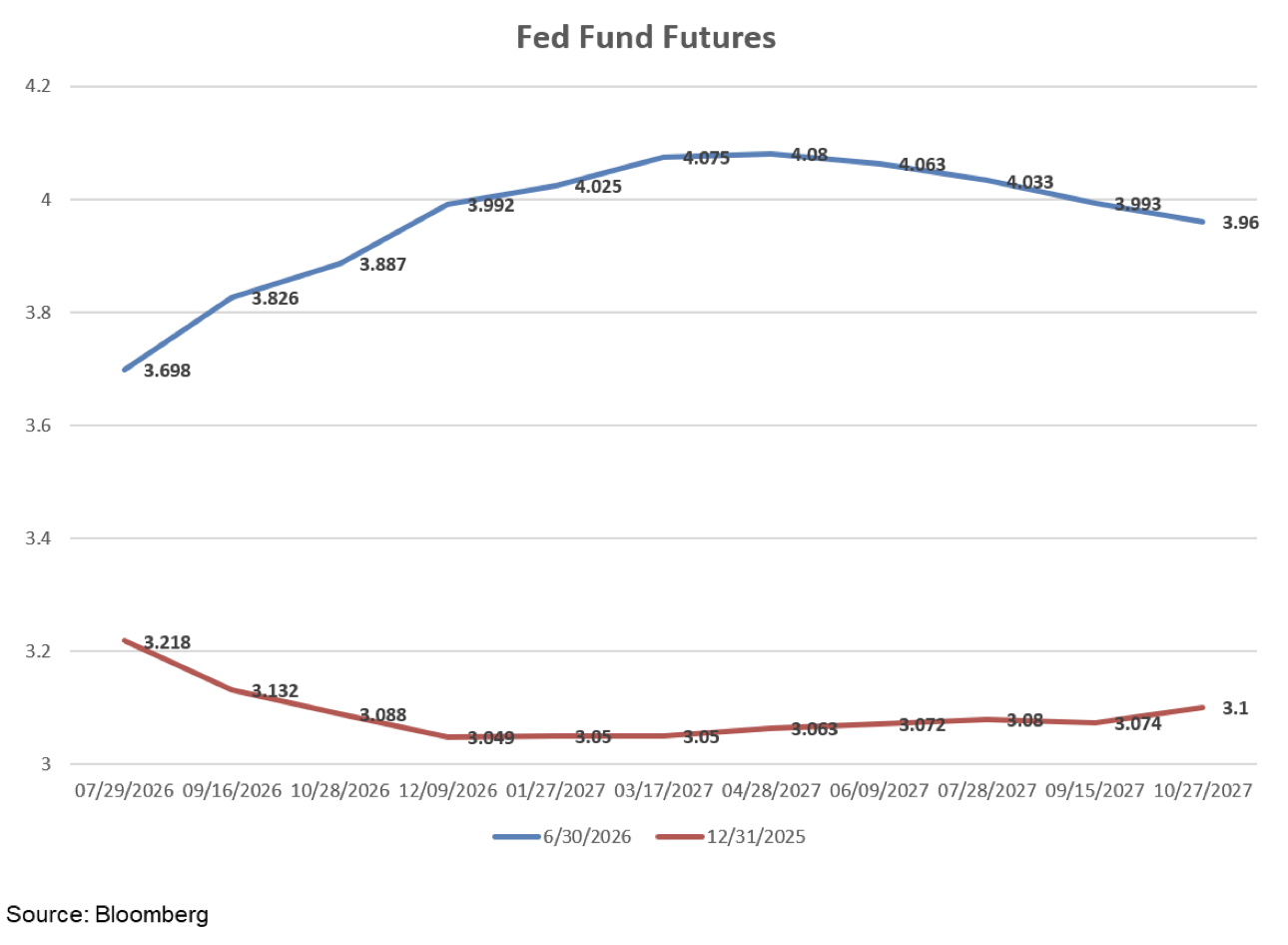

Faced with persistent inflation, the new Federal Reserve Chairman, Kevin Warsh, struck a decidedly hawkish tone. He underscored the Fed’s inflation target and role in delivering price stability while indirectly quelling any lingering fears regarding Fed independence. Financial markets have quickly pivoted, completely unwinding earlier expectations for near-term interest rate cuts. Instead, investors are now pricing in a higher-for-longer policy stance, including a potential rate hike later this year if price pressures do not cool.

Domestic inflation is being fueled by strong underlying economic growth, a stark contrast to international softness. Across Europe and the UK, business activity has visibly stalled, with Purchasing Managers’ Indexes (PMIs) slipping into contraction territory. By comparison, the U.S. manufacturing PMI hit a four-year high in May, boosted by companies aggressively stockpiling inventory to shield themselves from shipping delays. Even so, this stop-and-go backdrop creates a cloud of policy uncertainty, leaving many corporate leaders hesitant to commit to major, multi-year capital investment decisions, excluding AI-related projects.

Meanwhile, the American consumer continues to show a clear K-shaped split. Higher-income households continue to spend comfortably, insulated by a multi-year wealth effect from rising home values and stock portfolios. On the other side of the ledger, lower- and middle-income families are feeling the squeeze of high gasoline prices and dwindling personal savings. Providing a vital floor to the economy is the labor market, which remains steady with unemployment anchored at 4.3% and three months of consistent job creation exceeding 170,000 jobs per month.

The domestic housing market continues to flash mixed signals, reflecting ongoing affordability challenges. Mortgage rates remained elevated, keeping a tight lid on building activity as housing starts fell 2.8% in the quarter. Yet, pending home sales managed a 1.4% monthly bounce, demonstrating that underlying housing demand remains intact despite high rates and property values. Adding to this uncertainty, a proposed bill for housing relief has become ensnared in politics, delaying potential support for the residential real estate sector. Until the affordability issues are resolved, the housing market is likely to remain in a protracted holding pattern.

Equity Markets

U.S. equity markets marched through a barrage of geopolitical headlines to post exceptional gains, supported by robust corporate fundamentals. Aggregate earnings growth for the first quarter tracked at an impressive 29.9% year-over-year pace, driving widespread upward revisions to future analyst expectations. Propelled by these strong numbers, the S&P 500 advanced 15.2%, the Nasdaq grew 21.6%, the S&P 500 equal-weighted rose 11.4%, and the Dow Jones Industrial Index climbed 13.4% during the second quarter. Under the surface, investor sentiment underwent sharp, headline-driven swings. Widespread optimism surrounding temporary Middle East ceasefire talks routinely fueled rapid relief rallies, while unexpected diplomatic setbacks just as quickly triggered short-term pullbacks.

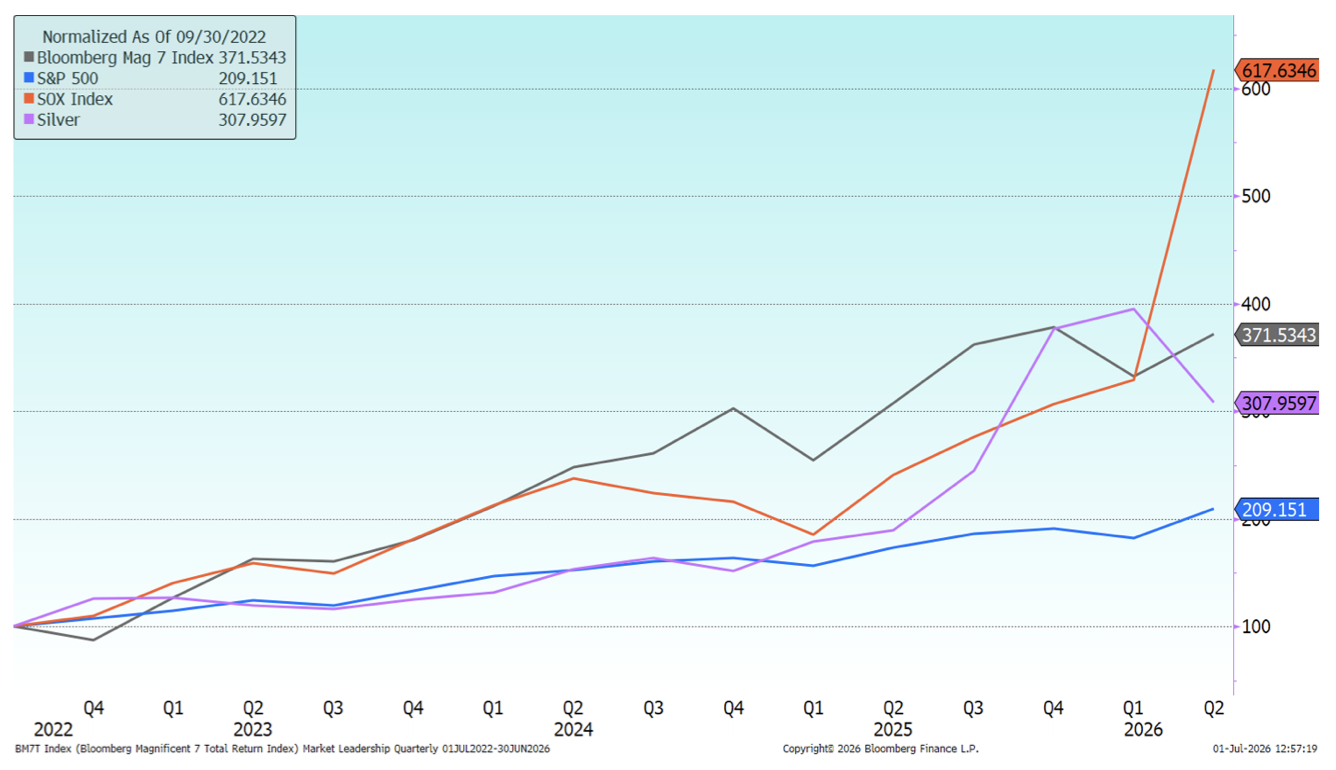

A defining feature of this market cycle remains its historically narrow breadth. While the initial leg of the April rally was led by the Magnificent Seven tech giants, this leadership shifted into semiconductor and related infrastructure stocks (like AMAT, ASML, and TSM). The PHLX Semiconductor Sector Index (SOX) surged over 80% in Q2, its best quarterly performance ever. This concentration has kept the S&P 500 at an elevated forward earnings valuation multiple of 20.2x, well above its 20-year average of 16.7x. At the same time, investor enthusiasm for the artificial intelligence ecosystem has spilled over into primary capital markets. Massive private venture capital flows continue to bankroll advanced machine learning startups, while anticipation builds around the expected mega-IPOs of high-profile industry pioneers like Anthropic and OpenAI.

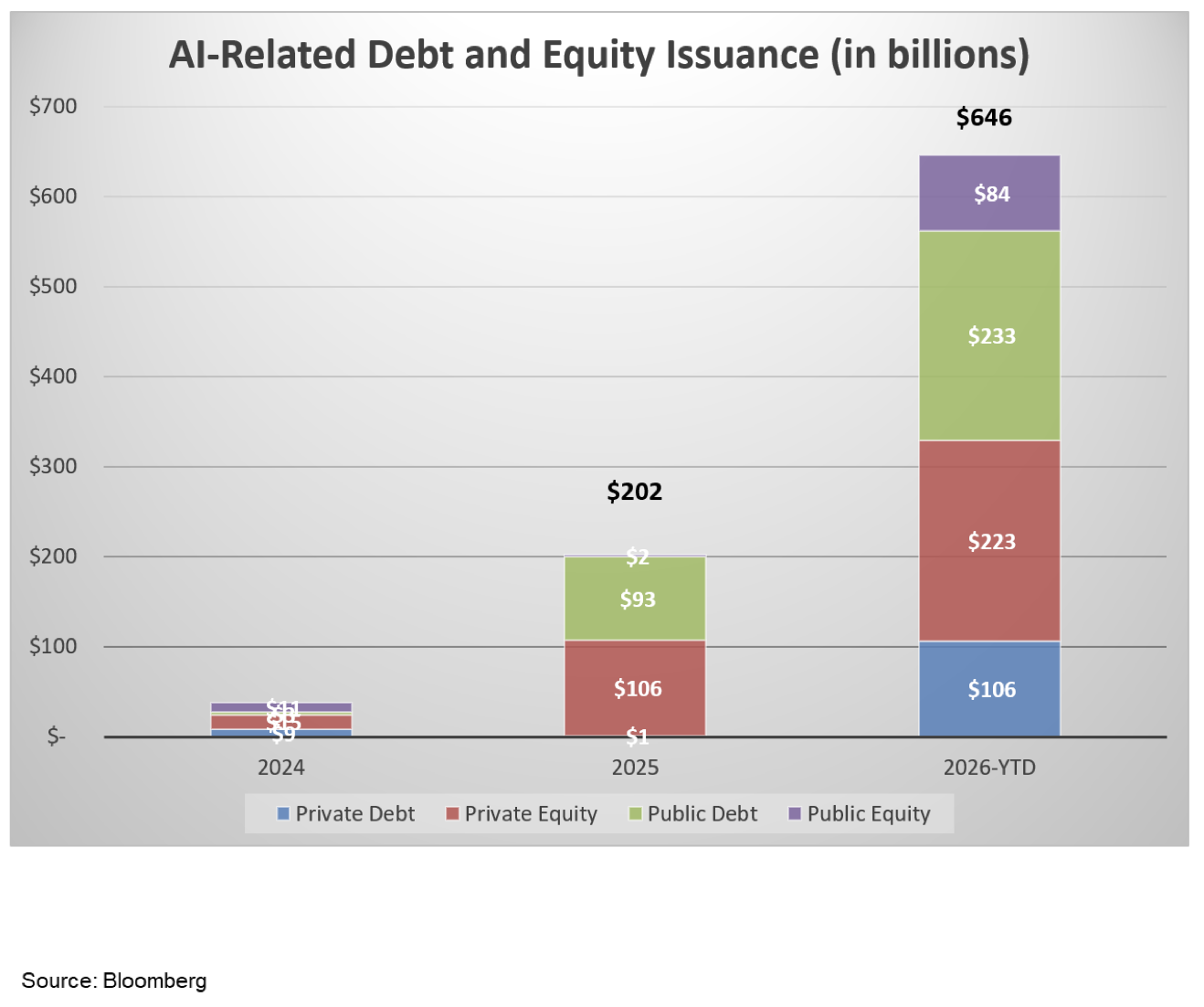

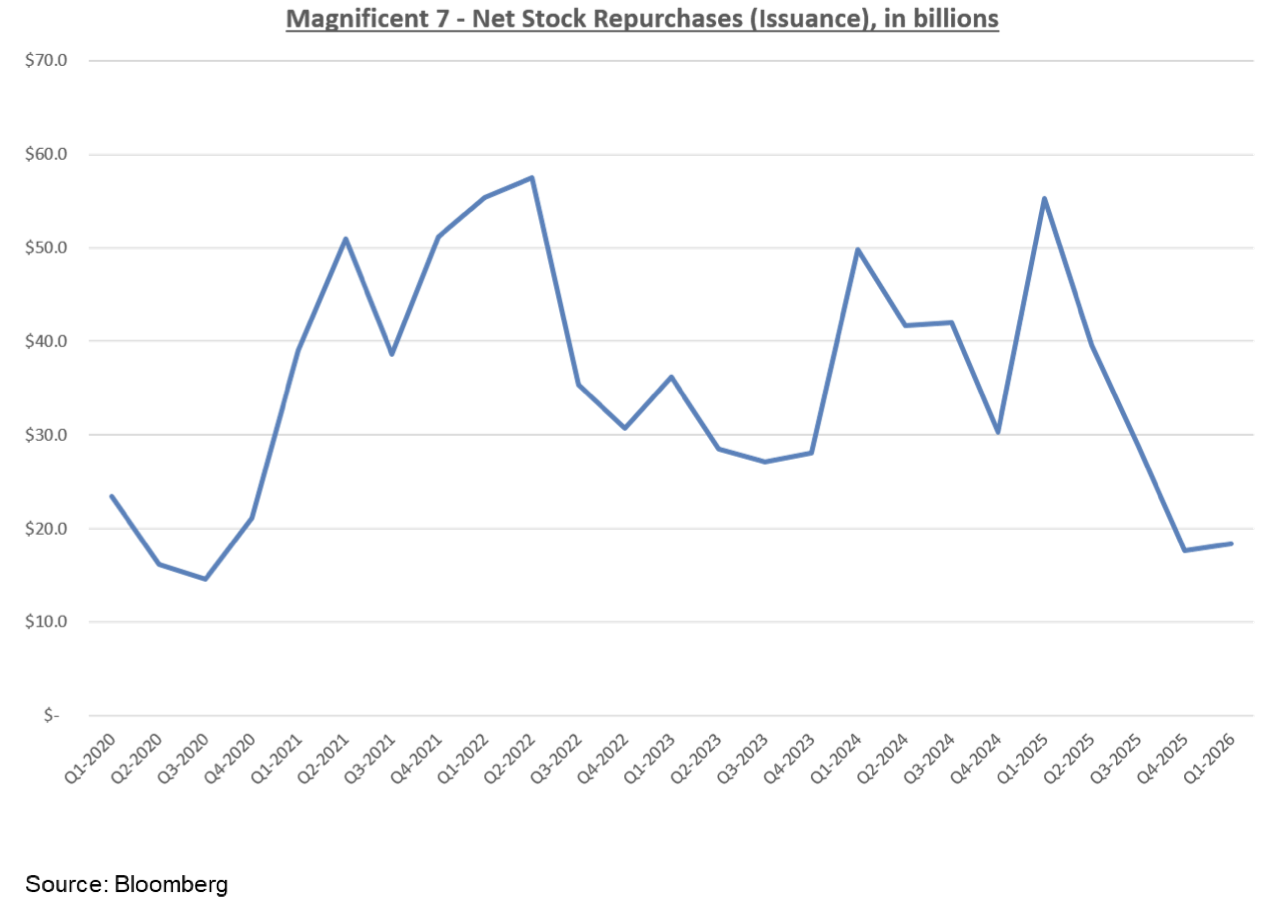

However, a significant structural shift is occurring in corporate capital management that warrants close monitoring. For years, corporate share repurchases provided a reliable tailwind for earnings-per-share growth. This quarter, we observed the initial stages of a reversal, as mega-cap technology companies began shifting away from buybacks and toward new equity issuance to fund their massive AI data-center capital expenditures. In addition to SpaceX’s $86 billion IPO, Alphabet raised $85 billion the week before, and other large-cap technology companies are rumored to be contemplating equity offerings while markets are receptive. While these massive spending projects are a powerful engine for general economic growth, the sheer volume of new shares coming to market represents a notable headwind to the per-share earnings power investors have come to expect. Given this backdrop of rich valuations and narrow leadership, our focus remains squarely on identifying fundamentally sound businesses that can compound cash flows and earnings without relying on financial engineering or excessive debt financing.

Fixed Income Markets

The fixed income landscape experienced an abrupt repricing this quarter as the Treasury yield curve adjusted to the reality of stickier inflation and a more hawkish Federal Reserve. The more policy-sensitive 2-year Treasury yield rose over 30 basis points (bps) to 4.1% during the quarter as the market digested the prospects of a potential rate hike. The benchmark 10-year Treasury yield surged above 4.6% in mid-May, settling at 4.4% at quarter-end as investors priced in the credibility of the central bank’s ability to rein in inflation over time. This combination of moves flattened the yield curve, with the spread between 2-year and 10-year yields narrowing from 55 bps to 27 bps over the quarter.

This volatile bond backdrop directly traces back to the leadership transition at the nation’s central bank. Following the conclusion of Jerome Powell’s term on May 15, Kevin Warsh officially began his tenure as the new Chairman. At his debut FOMC press conference in June, Chair Warsh began his anticipated shift in Fed communications, delivering a highly abbreviated policy statement that stripped out forward guidance. For investors, this new operational style implies less transparency going forward, as the central bank moves toward an explicitly data-dependent posture that leaves the market to interpret each inflation print independently.

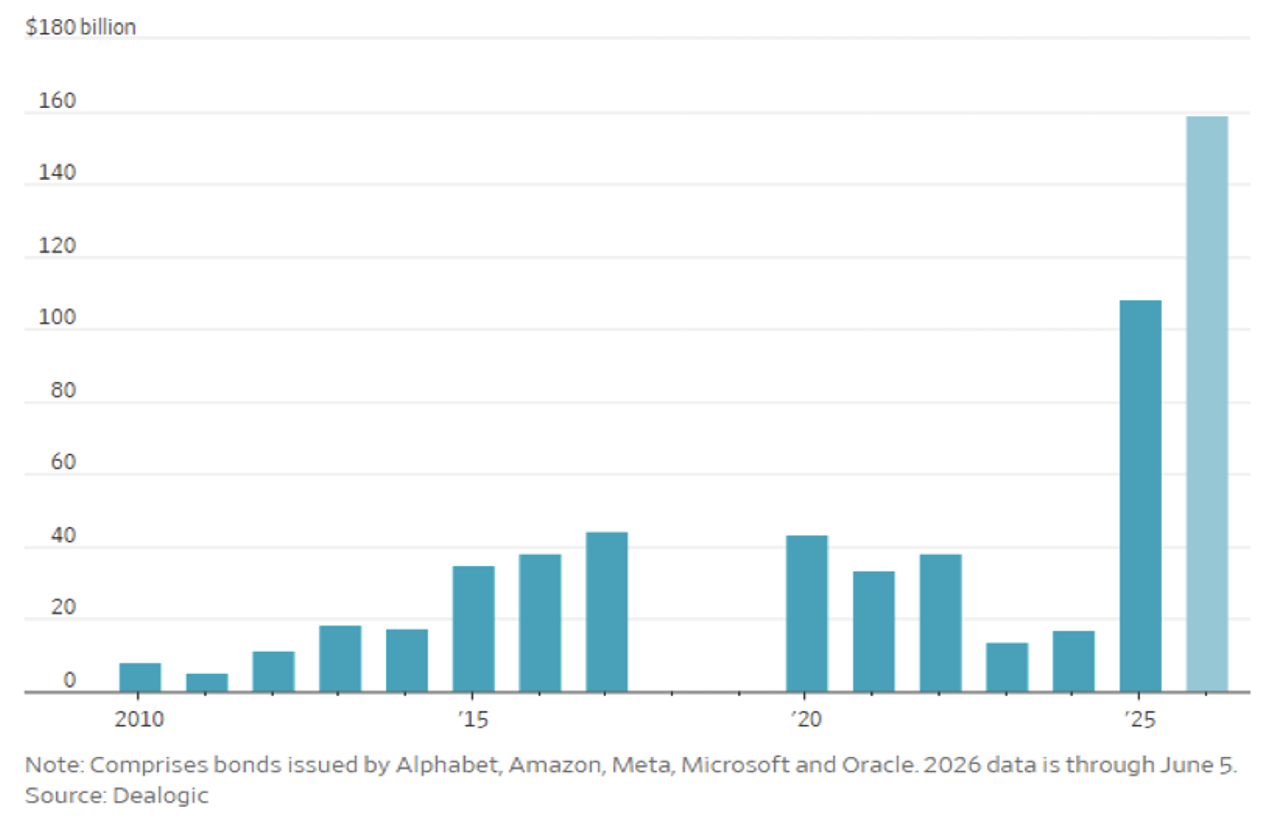

Despite the upward reset in Treasury yields, traditional corporate credit markets showed incredible resilience. Investment-grade and high-yield bond spreads remained remarkably tight, held in check by modest default rates and healthy cash positions. Management teams are taking advantage of this, with the market seeing a significant wave of new debt issuance to fund massive, long-term AI infrastructure projects. Bloomberg estimates that over $400 billion of debt capital has been raised in 2026 for AI projects. Companies including Amazon, Alphabet, and Oracle raised over $100 billion of debt in Q1, and additional issues from Alphabet and Meta in Q2 bring that total to over $150 billion year-to-date.

The area we are watching in corporate credit is a potential deterioration in credit underwriting. The primary example of this is SpaceX’s post-IPO debt offering. The company raised $25 billion, and three credit rating agencies assigned investment-grade ratings to this debt, despite the company’s negative free cash flow and earnings. The issues have sold off slightly, particularly on the longer-dated maturities, which provides some comfort that markets are behaving properly. We are monitoring this to see if it is a one-off exception or if lower-quality companies can achieve comparable results. Another part of the market we continue to watch is private credit. These funds typically are structured with quarterly redemption windows, and stories of funds capping these distributions have begun circulating again, raising concerns over the health of these loan books and fear of negative ripples through credit markets. Our approach continues to emphasize credit quality and building customized, laddered bond portfolios with intermediate average duration. This strategy allows our clients to secure high current income and protect principal without chasing yield in opaque private markets.

Conclusion

The second quarter served as a reminder of the importance of balance and high-quality underlying assets when facing periods of heightened disruption and volatility. A complex mix of persistent inflation, narrow equity market breadth, policy shifts, and rising fiscal deficits will likely keep market volatility elevated. The investment playbook from the last three to four years, which relied on passive index concentration, faces a real test in this higher-for-longer interest rate environment. At Guyasuta, our time-tested strategy remains disciplined and focused on the fundamentals when constructing resilient equity and fixed income portfolios. This helps our clients navigate these macroeconomic crosscurrents with confidence, as we aim to preserve capital, grow your wealth, and deliver reliable income tailored to meet each of your individual financial goals and needs. As always, we look forward to serving you and addressing any of your questions.

Market leadership has rotated from Mag 7 to semiconductor stocks

Increased capex spending by tech companies has reduced buybacks

PCE headline inflation is headed in the wrong direction

Gasoline prices remain high, while oil has dropped over the last month

Market expectations for Fed Funds have shifted from the beginning of the year

Global bond issuance by big AI tech companies