Summary

The first quarter of 2026 introduced new complexities to an economy that previously seemed destined for a soft landing. While 2025 was defined by remarkable resilience and steady growth, the early months of this year have been shaped by a sharp energy supply shock stemming from escalated conflict in the Middle East. This has forced a shift in the market narrative from monetary easing toward inflationary vigilance, as investors begin to weigh the risks of a challenging environment defined by stagnant growth and stubbornly high prices. Despite these headwinds, the U.S. economy continues to show unique durability, supported by its domestic energy production and a robust corporate sector. In this edition of the Market Comments, we will examine the evolving geopolitical landscape and trade policies, the sustainability of current economic growth, the core drivers within the equity markets, and the shifting fixed income landscape.

The Economy

The U.S. economy entered 2026 facing a sudden stress test as the optimism of the previous year gave way to renewed geopolitical friction. Navigating the interplay between energy spikes and domestic price stability is now the primary task for investors, as these factors dictate the cost of money for everything from corporate loans to personal mortgages. Despite this challenging macro backdrop, the domestic landscape remains a study in relative resilience, bolstered by expansive data center investment and a steady industrial core. Both ISM Manufacturing and Services readings remain above 50, a level indicating continued economic expansion. The underlying economy continues to demonstrate fundamental strength despite inflation headwinds, sustained by robust domestic energy production and a consumer base that has, thus far, weathered an evolving policy landscape.

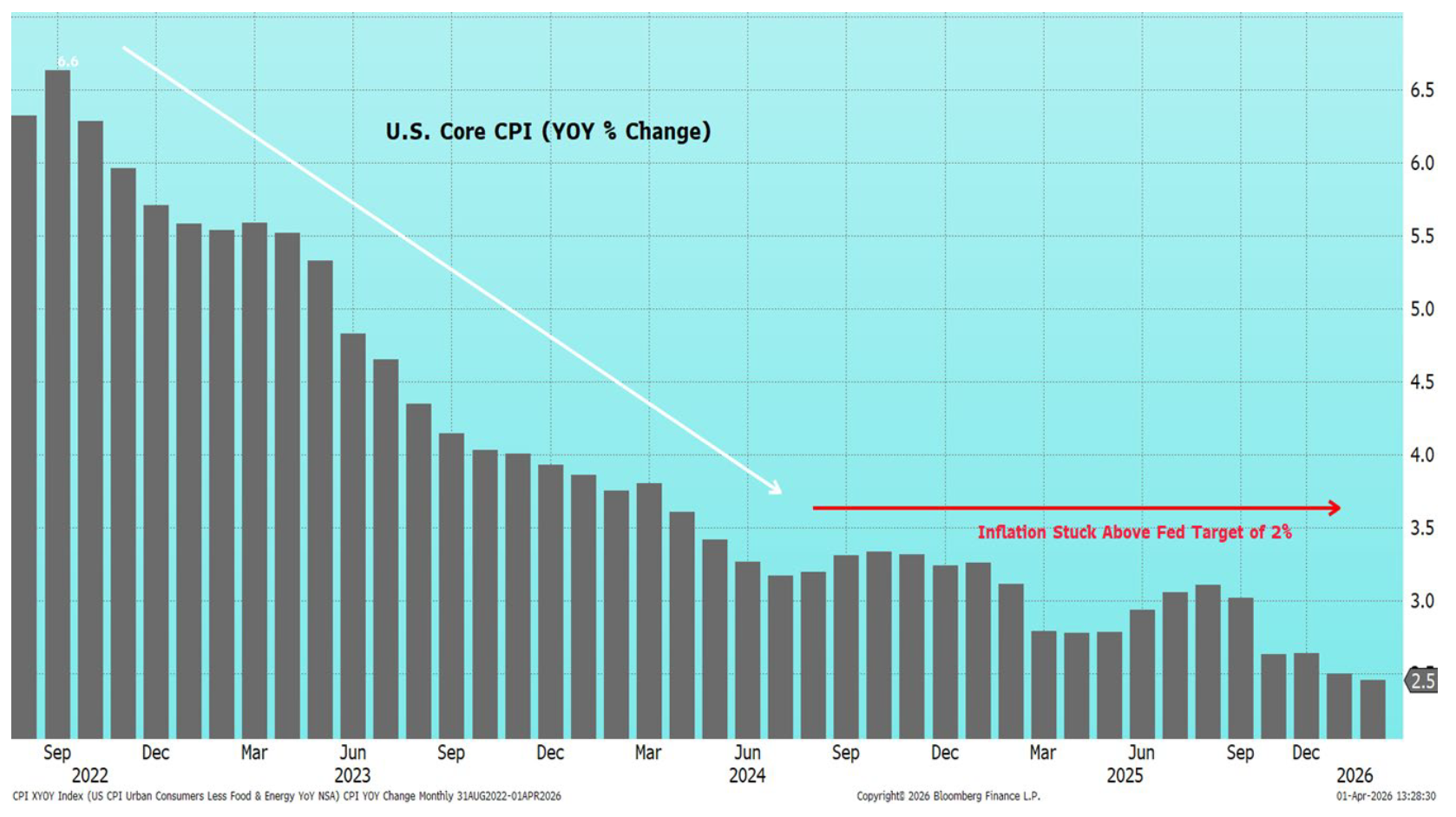

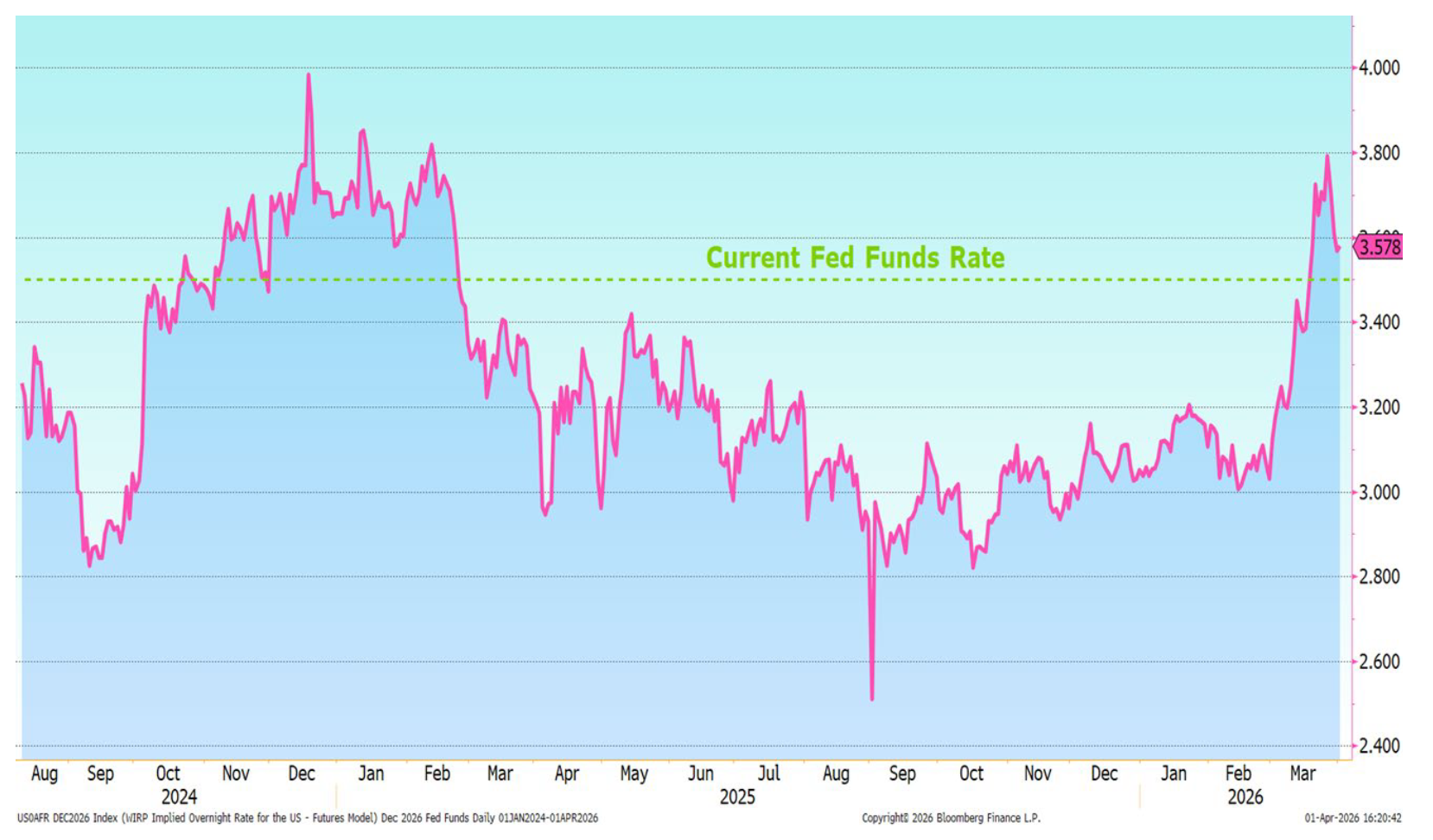

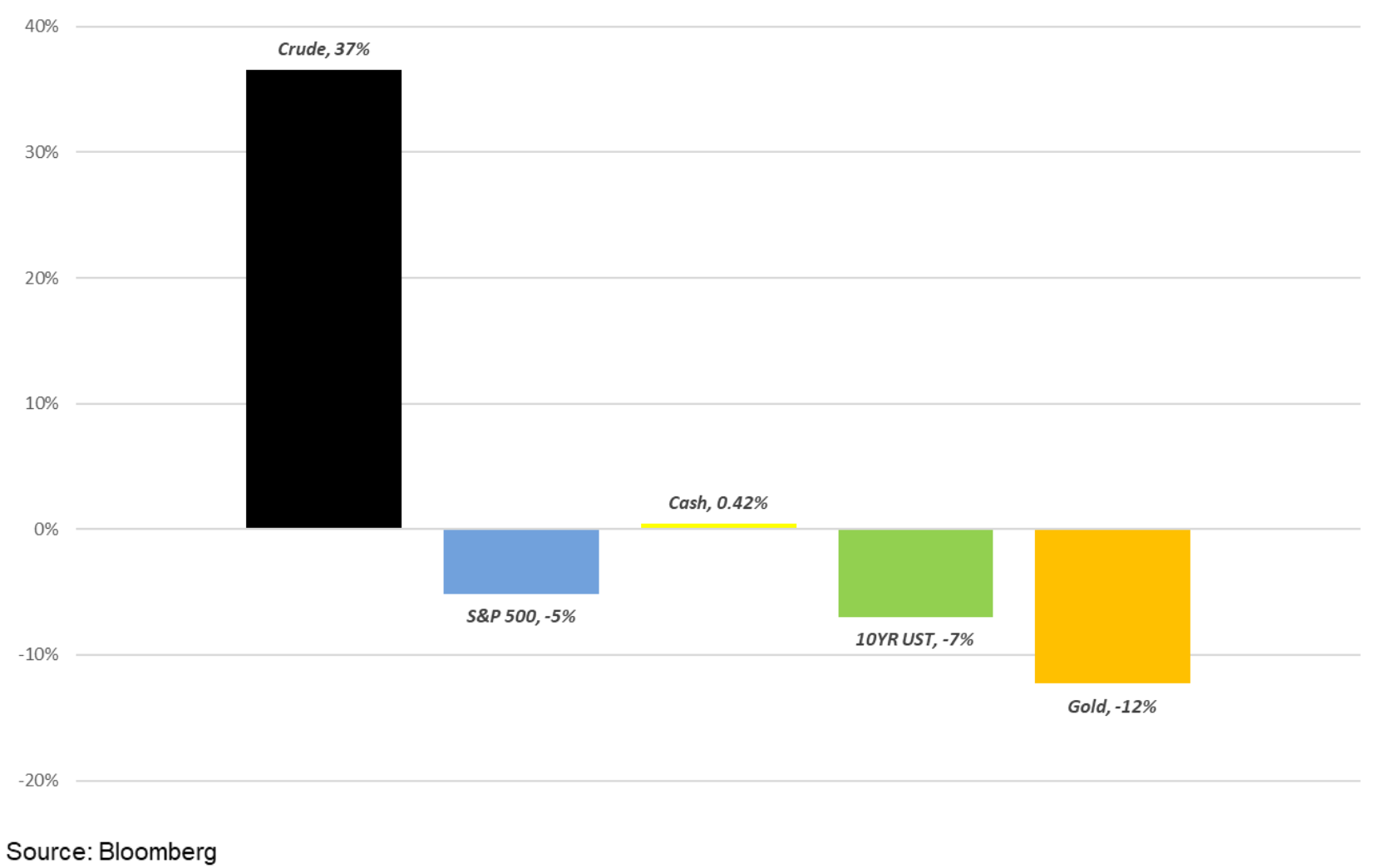

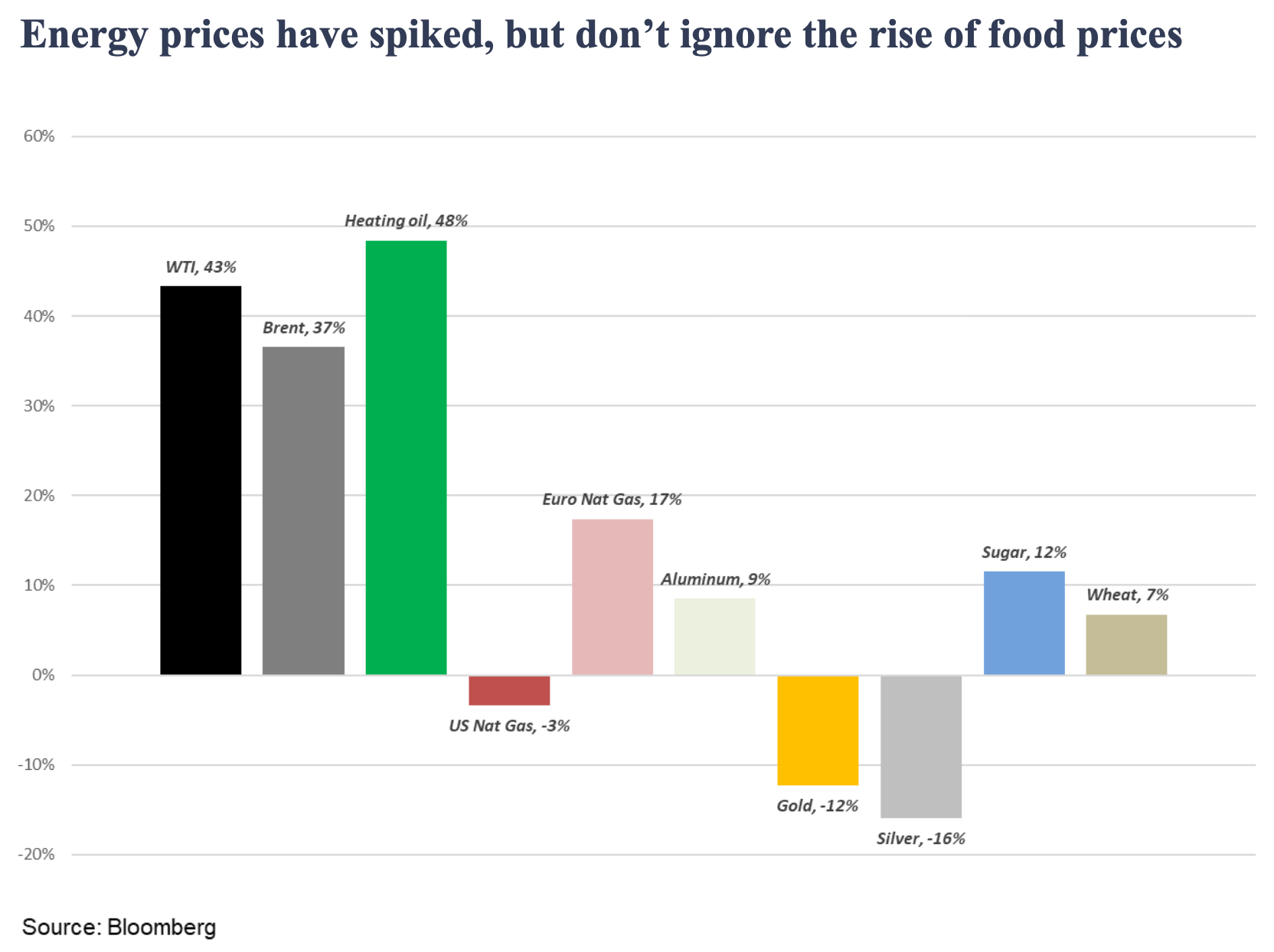

The primary driver of economic shifts this quarter was the Middle East conflict, which drove oil prices up roughly 40% in March. This represents a significant supply shock that ripples through the economy by raising costs for transportation and manufacturing. While headline inflation had cooled to 2.4% early this year, more recent PCE (Personal Consumption Expenditures) data has run hotter at 3.1%. This shift has prompted the Federal Reserve to raise its year-end inflation projections, and, consequently, officials have hit the pause button on cuts, holding the benchmark rate at 3.50% to 3.75%. Markets have effectively priced out that expectation for 2026, pivoting toward a higher for longer stance as renewed energy-driven inflation remains a primary concern.

Recent data prints have introduced new variables to the economic narrative, notably with U.S. 4Q25 GDP growth revised down to 0.7%. While a single data point does not make a trend, the combination of slowing growth, persistent softness in the housing market, and the recent energy shock has led some economists to raise the probability of a recession in the next 12 months. This observation comes alongside a complex policy backdrop. For example, the Supreme Court recently struck down the use of emergency powers (IEEPA) for certain tariffs, yet the administration is already pursuing alternative legal avenues to reimpose them. This stop-and-go trade policy creates a cloud of uncertainty for businesses trying to forecast future costs. However, the U.S. maintains a structural advantage in this environment because of its energy independence. Unlike Europe or Asia, which are grappling with severe Liquid Natural Gas (LNG) import disruptions, U.S. domestic production acts as a partial shock absorber against the global volatility that might otherwise bring growth to a standstill.

The current economic backdrop highlights a critical transition from growth-at-any-cost to an environment where innovation, efficiency, and energy independence are the primary competitive advantages. For our clients, this means the historical playbook of low-interest rate investing is being rewritten. The era of easy money that prioritized scale over sustainability has been replaced by a market that favors companies with the cash flow to fund their own operations. We are closely monitoring the pass-through effects of higher oil. If energy prices remain at high levels, they act as a de facto tax on the consumer, potentially slowing retail sales which were a pillar of 2025’s strength. This risk is complicated by the K-shaped nature of the current economy, where the resilience of higher-income households, bolstered by a multi-year wealth effect from rising home and equity values, contrasts with the mounting pressure on price-sensitive consumers. However, the structural shift in the labor market, stemming from AI-driven productivity gains, may provide a necessary buffer against these inflationary pressures, allowing corporate margins to stay firm despite the rising cost of inputs. The takeaway is that the stagflationary undertone, where growth slows while inflation pressure builds, has become a key risk.

Equity Markets

Equity markets have undergone significant internal volatility this quarter, as the tide of easy momentum investing gave way to a more discerning focus on old economy, staples, energy, and physical infrastructure stocks. While broad market indices often mask underlying volatility, a look beneath the surface reveals a healthy rationalization of valuations and a move away from extreme concentration. This rising dispersion, the difference in performance between individual stocks, is creating a landscape where fundamental quality and company-specific results are increasingly the primary drivers of portfolio returns.

Through the close of the quarter, the major averages reflected this cautious environment, with the S&P 500 declining 4.3%, the Nasdaq Composite falling 7.1%, and the Dow Jones Industrial Average off 3.2%. While these indices remain relatively stable with only single-digit drawdowns, there is significant movement within the sectors. The extreme concentration that has defined this cycle, where just ten mega-cap stocks account for over 30% of the S&P 500’s total market capitalization, is being tested by a more discerning investor base. We have seen a notable repricing of AI-exposed traditional industries as investors worry that new technology could pressure profit margins through increased competition or the total disruption of legacy services. Conversely, most of the pick-and-shovel plays, the semiconductors and electrical components required to build the physical AI infrastructure, have remained positive. The energy sector has been the standout leader, rising nearly 40% year-to-date and providing a necessary offset to broader equity weakness, though it continues to represent a modest 4% weighting within the S&P 500.

Pairwise correlation measures how closely individual stocks move in the same direction. A significant trend this quarter is the drop in the S&P 500’s 3-month pairwise correlation to nearly 10%, one of the lowest levels since 2022. A low reading indicates that performance is being driven more by a company’s specific fundamentals than by broad market sentiment. Notably, this environment has allowed small-cap stocks to outperform large-caps year-to-date, as investors seek more domestically focused companies and undervalued segments of the market. This broadening of market participation is a constructive development, as it suggests that the current market cycle is being supported by a wider array of American businesses, providing a healthy diversification of leadership as investors navigate the latest batch of economic data.

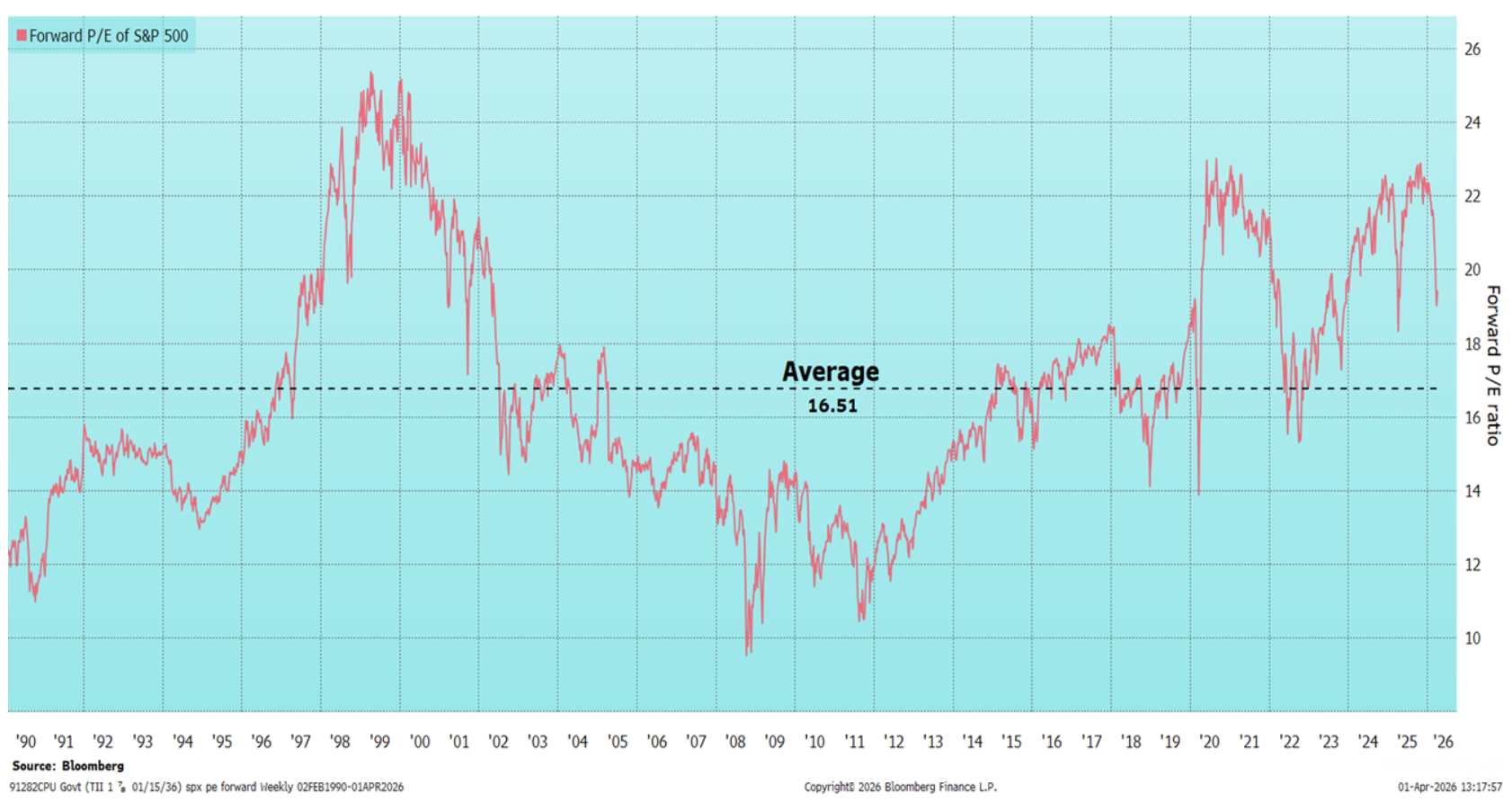

This shift in market leadership is particularly evident in the transition from speculative AI applications toward the tangible assets that power them. Investors are increasingly prioritizing companies that possess physical moats, such as specialized manufacturing capabilities or utility and energy infrastructure solutions, over those that merely offer digital tools. This flight to reality is a rational rebalancing, as it rewards businesses with durable cash flows and the ability to navigate an environment where the cost of capital is no longer zero. We see this reflected in broader market valuations, as the S&P 500 next twelve months forward P/E ratio has moderated to 19.9x from the more elevated levels seen late last year. With market valuations cooling, investors are becoming more selective, favoring companies that deliver tangible results and generate sufficient cash to fund their own growth without needing to borrow at today’s higher interest rates.

At Guyasuta, our investment framework remains anchored in the same core principles of quality and fundamental strength. While market leadership may rotate, our focus is on identifying companies with durable competitive moats and consistent free cash flow. We continue to prioritize businesses with the pricing power and balance sheet health necessary to navigate shifting economic data without compromising their long-term objectives. This disciplined approach, including a strategic underweight to the Magnificent Seven, has highlighted the structural benefits of diversification as investors look beyond index concentration for value. By maintaining a diversified portfolio of high-quality companies, we aim to participate in growth while mitigating the impact of volatility.

Fixed Income Markets

Fixed income markets underwent a significant repricing this quarter as the lower for longer rate narrative encountered a reality check. For much of late 2025, markets had priced in a steady cadence of rate cuts, but persistent inflation data, complicated by the surge in energy costs, has forced a recalibration of those expectations. At Guyasuta, we continue to manage this portion of the portfolio as a foundational anchor, prioritizing liquidity and capital preservation.

The 10-year Treasury yield climbed back toward the 4.3% to 4.4% range during the quarter as the market adjusted for a Federal Reserve that may remain on hold longer than previously anticipated. This upward pressure on yields has challenged the traditional safe haven status of long-term bonds. Consequently, we have maintained a disciplined stance on duration, favoring shorter-to-intermediate maturities. This positioning allows us to capture attractive current yields while remaining less sensitive to interest rate swings that can impact the principal value of longer-dated bonds.

Beyond the movement in rates, we are closely monitoring the impact of sustained borrowing costs on the broader economy. With U.S. 30-year mortgage rates hovering around 6.3%, credit-sensitive sectors like housing remain in a period of subdued activity. While high-quality corporate balance sheets remain generally healthy, we are continuing to watch for signs of systemic stress in the $3 trillion private credit market. The current complexity and lack of transparency in these private markets share notable characteristics with the mortgage-backed securities that preceded the 2008 financial crisis. Recent redemption halts and withdrawal limits among major alternative asset managers serve as a potential precursor to broader credit contagion, a reminder that in opaque markets, isolated instances of distress are often indicative of deeper, underlying pressures. Our strategy avoids these frothy segments, focusing instead on investment-grade issuers and government-backed securities that provide a predictable stream of income. Our fixed income approach remains rooted in the same principles as our equity philosophy: a commitment to quality and durability. By focusing on issuers with the cash flow to easily service their debt in a higher-rate environment, we ensure that bond allocations provide the necessary stability to offset equity market fluctuations. We continue to monitor the evolving inflation outlook and the Federal Reserve’s response to the latest economic data, ensuring our positioning remains aligned with the long-term objectives of the portfolio.

Conclusion

As we conclude the first quarter of 2026, the primary theme across markets is one of heightened vigilance and risk management. The convergence of volatile Middle East tensions and a recalibration of domestic growth expectations underscores the importance of our long-standing commitment to fundamental analysis. While we remain vigilant regarding the early signs of stress in credit and housing markets, our strategy remains anchored in the belief that quality, durability, and robust cash flows are the best defenses against cyclical uncertainty. We appreciate the trust you place in us to manage your investments and look forward to the year ahead.

S&P 500 forward P/E ratio has fallen since January, but is still above the long-term average

Inflation remains above the Fed’s 2% target

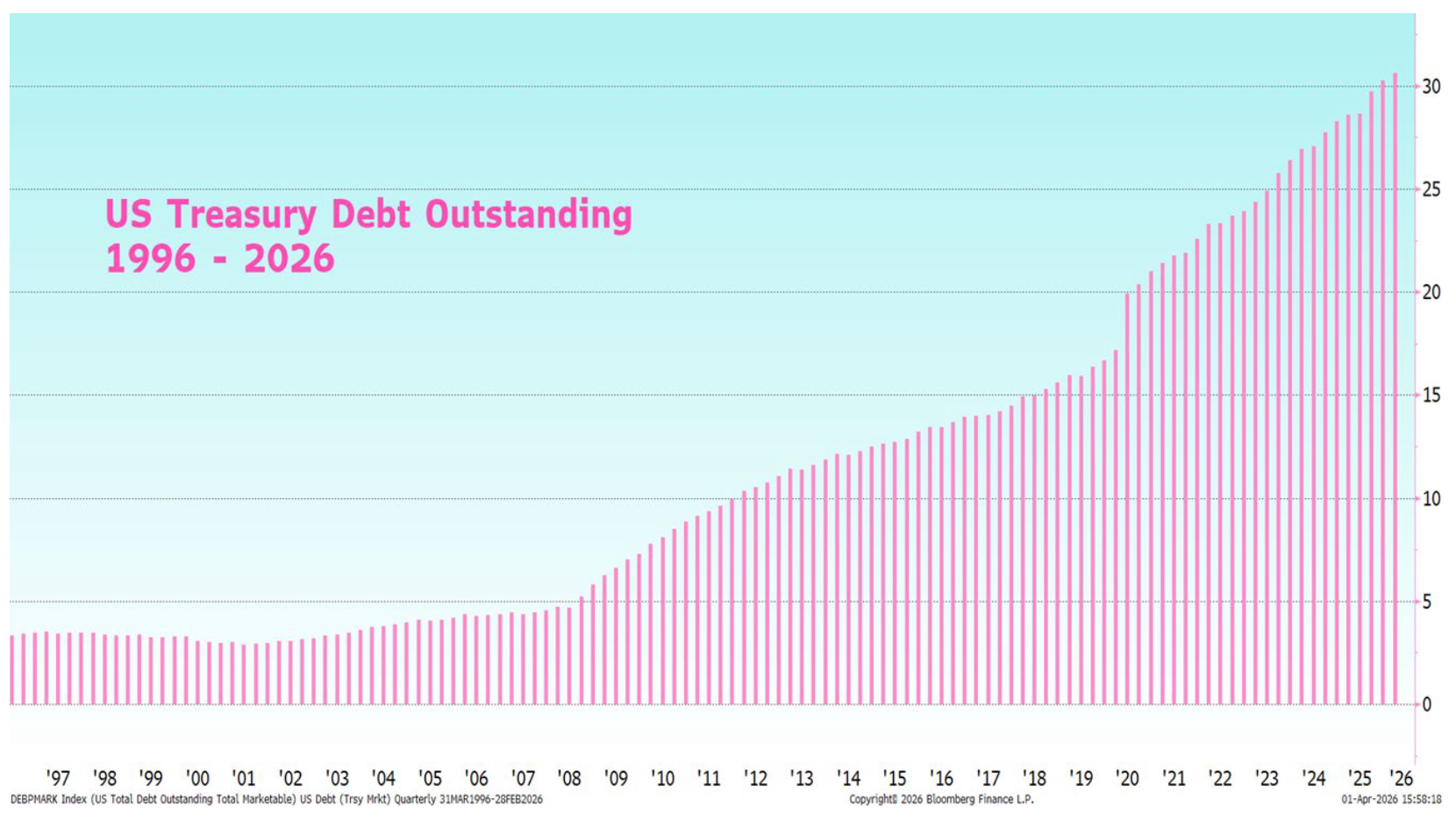

U.S. Treasury debt has grown 6x in 30 years

Expected Fed Funds rate for December 2026

Asset class performance in March: oil and cash positive with stocks, bonds, and gold negative

Energy prices have spiked, but don’t ignore the rise of food prices

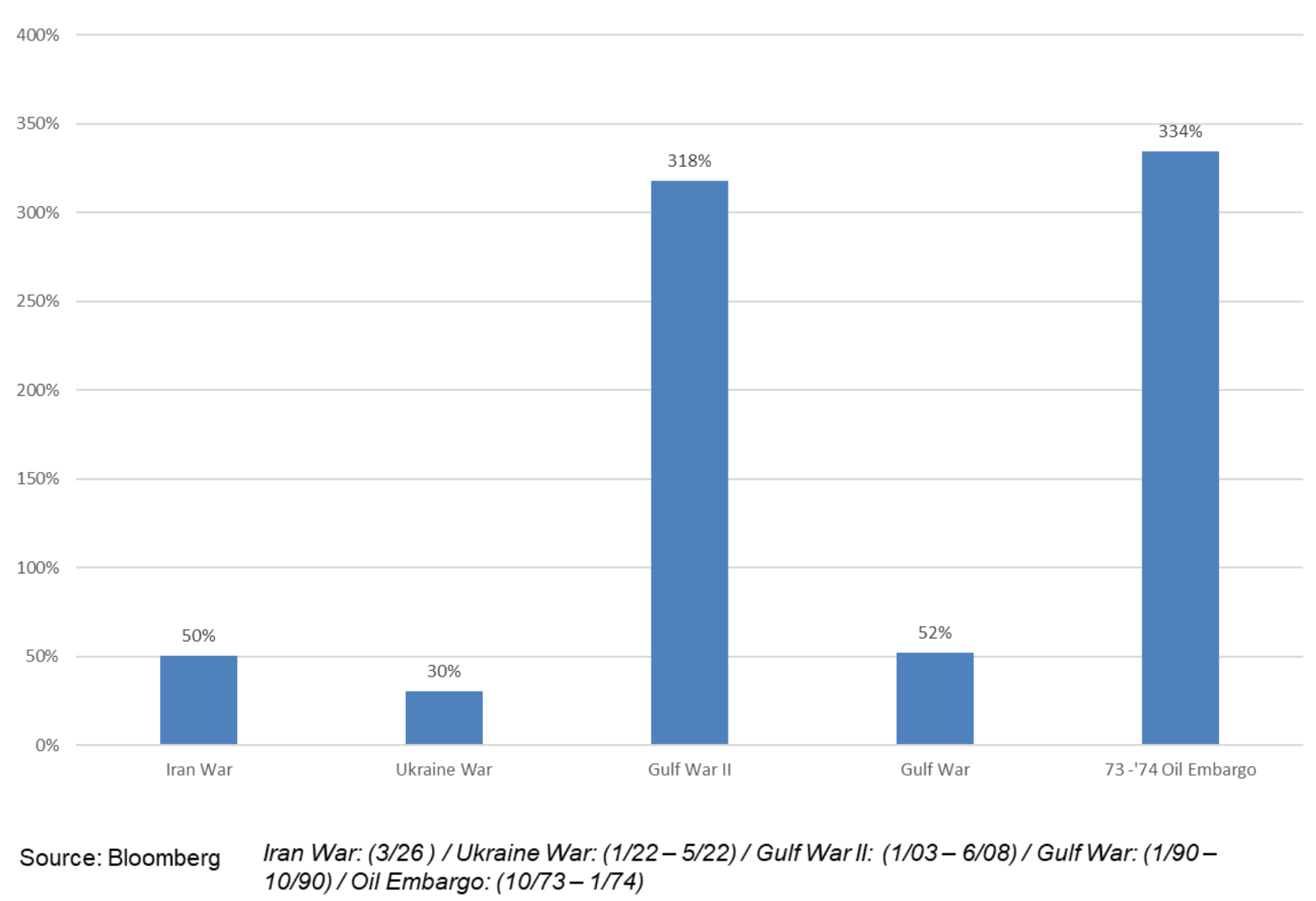

Oil prices spikes over the years

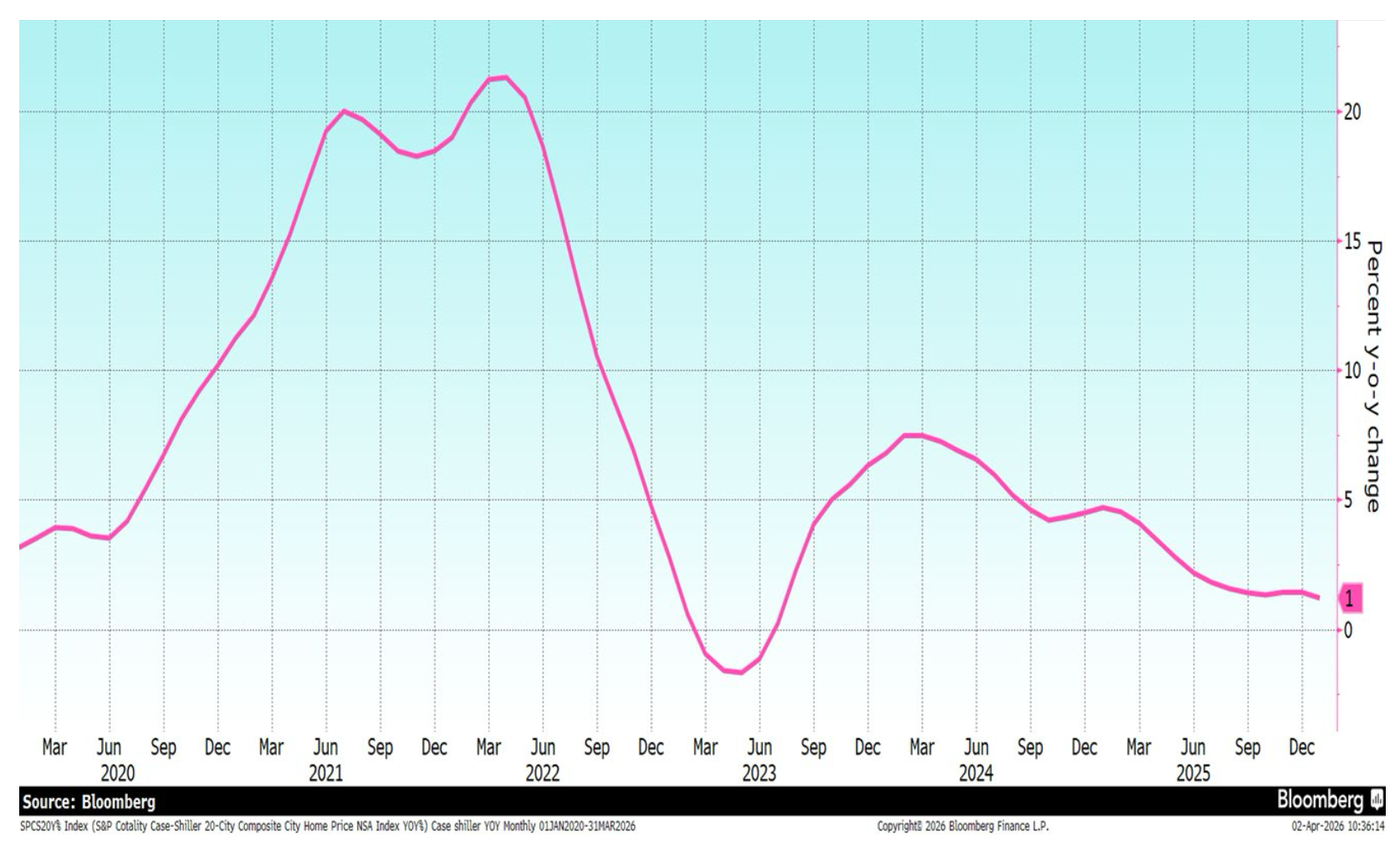

Case Shiller Index shows housing prices have leveled off