Summary

In the third quarter of 2025, markets responded to changes in monetary policy and the economic landscape. The Federal Reserve delivered its first rate cut since December 2024, citing labor market softening, while signaling additional easing ahead. With inflation remaining stubborn, the threat of stagflation is an ongoing concern. Equity markets proved resilient amid volatility, supported by strong earnings and continued enthusiasm around artificial intelligence (AI). Fixed income markets responded to the Fed’s dovish pivot with greater demand for quality and yield. Against this backdrop, we maintain a disciplined, diversified approach focused on long-term goals amid a maturing cycle.

The Economy

The U.S. economy showed signs of transition in the third quarter, with slowing labor conditions, persistent inflation, and new trade headwinds shaping the outlook for the remainder of 2025 and beyond. In a notable shift, the Federal Reserve cut the Federal Funds rate by 25 basis points, moving the target range to 4.00%–4.25%, its first cut since the fourth quarter of 2024. The Fed cited “slowing job gains and a rising unemployment rate” as key rationale for their decision. The median forecast now projects two additional cuts by year-end, potentially bringing the Federal Funds rate down to 3.70% by December. This marks a turning point in policy, reflecting the Fed’s renewed focus on the employment side of its dual mandate: to manage inflation and support full employment.

Labor market conditions remain relatively strong by historical standards but have begun to soften at the margins. The unemployment rate ticked up from 4.10% to 4.30% in the quarter, and job openings have declined steadily over the same period. A shrinking labor force due to demographics and lower immigration has also reduced hiring flexibility for employers, particularly in services and healthcare. Wages continue to grow, though more moderately, with year-over-year increases slowing to just under 4.00%, which is still outpacing inflation. The Fed appears to be interpreting these trends as signals of a softening labor market. The scarcity of manual and technical workers is a key challenge, exposing companies to wage inflation and pressuring profit margins.

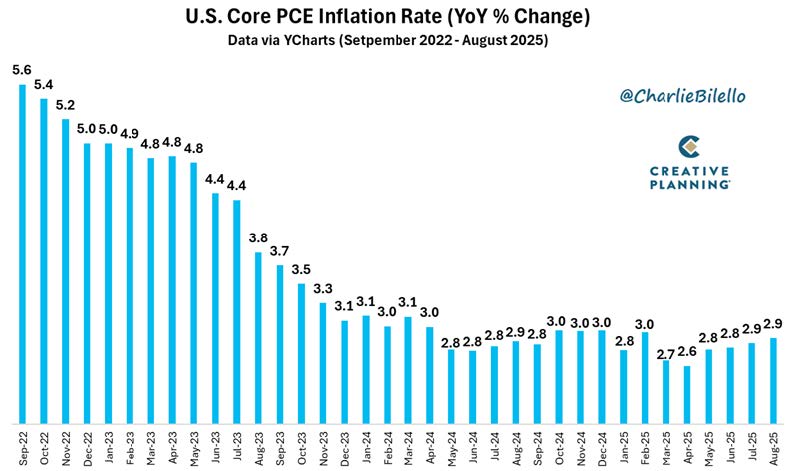

For both corporations and consumers, inflation remains a stubborn economic headwind. The core personal consumption expenditures (PCE) index continued to rise at a 2.90% annual rate in August, up from 2.80% last quarter, underscoring sticky price pressures in services and housing. While goods prices have stabilized, rising input and producer costs, partly driven by shifting tariff policies, are starting to filter into consumer prices. The risk of stagflation, where inflation remains elevated amid slowing growth, continues to garner attention among investors and economists alike.

The reintroduction of U.S. tariffs on global trade partners has reshaped trade expectations. Targeted sectors include pharmaceuticals, autos, electronics, agriculture, forestry, and mining, among others. These measures have triggered shifts in fiscal and monetary policy across affected countries, including surprise rate cuts and targeted stimulus for export-driven industries. While the direct impact on U.S. GDP is modest thus far, U.S. farmers have been negatively affected along with multinational companies that have exposure to China. U.S. CEOs privately comment that given the trade uncertainties it is difficult to make long-term capital investment decisions. Their concern is that trade policies could change with the current administration and then change again after the next Presidential election.

Consumer spending remains resilient but increasingly unequal. The top 10% of income earners continue to account for nearly half of all consumer outlays, a dynamic that amplifies the economy’s sensitivity to financial markets and wealth-driven consumption. Higher interest rates have weighed more heavily on middle-and lower-income households, who face rising credit card balances and declining savings. Mortgage rates fell in the quarter from 6.8% on the 30-year fixed to 6.3% at quarter-end. Despite the favorable move, housing activity remains soft. New home construction slowed, and affordability challenges persist, particularly in coastal and high-cost regions.

In short, Q3 highlighted a pivot point from an inflation-centric policy to one more focused on balancing risks. While the Fed has initiated its easing cycle, challenges remain, including persistent inflation, evolving trade policy, and a cooling labor market. These dynamics have the potential to recalibrate macroeconomic assumptions and introduce asymmetries in risk pricing, requiring greater selectivity and discipline in portfolio positioning.

Equity Markets

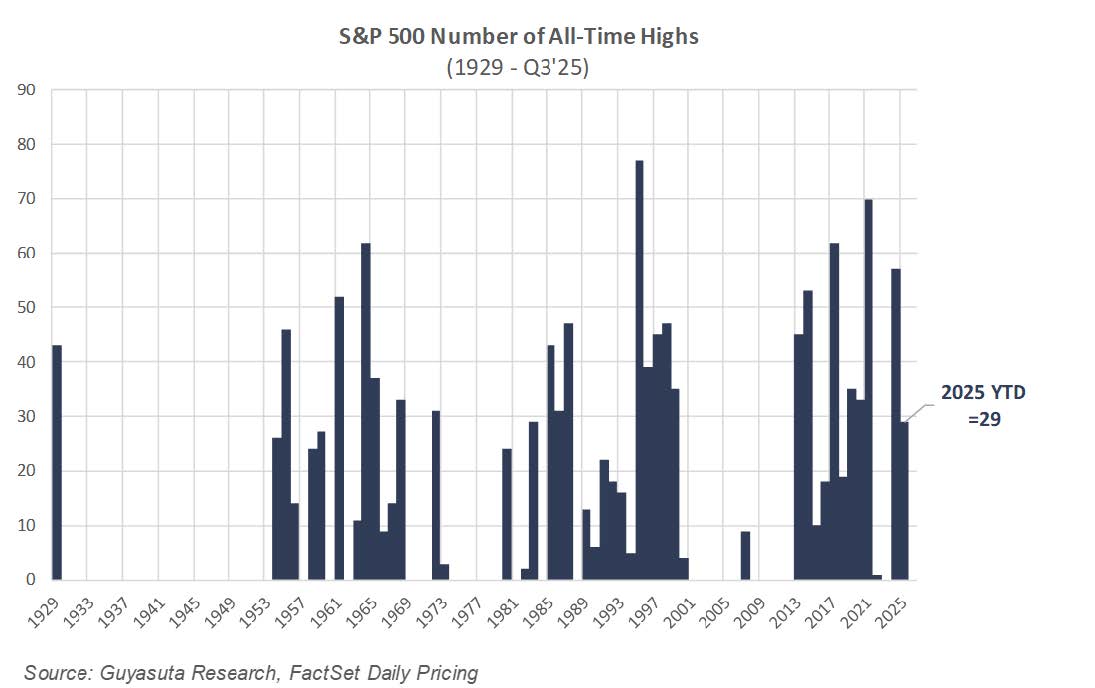

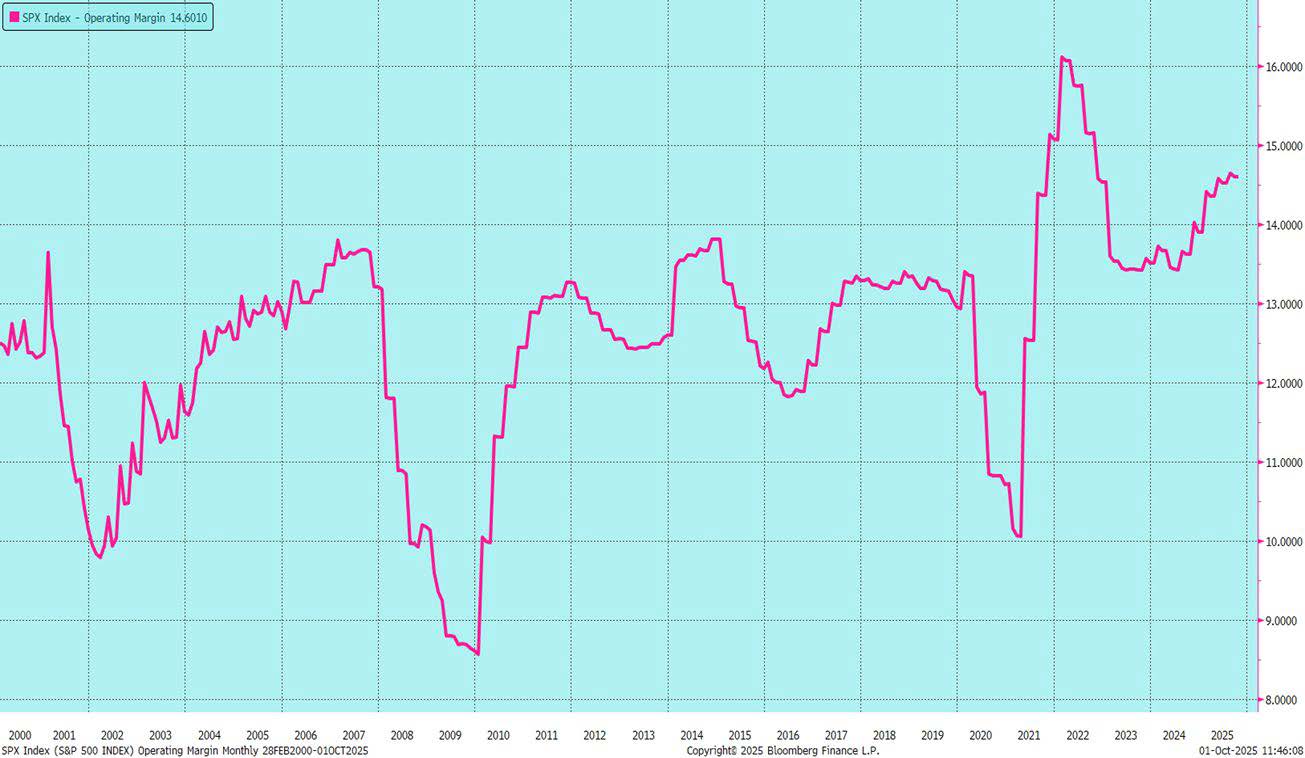

Equity markets posted solid gains in the third quarter, reflecting resilience amid a complex macroeconomic backdrop. Major indices were supported by robust corporate earnings, renewed investor enthusiasm, and continued strength in key growth sectors. The S&P 500 advanced 8.1%, the Nasdaq rose 11.4%, and the Dow Jones Industrial Average gained 5.7%. The ongoing adoption of artificial intelligence (AI), cryptocurrencies, and transformative healthcare innovations, such as weight-loss breakthroughs, has elevated disruption risks. Investor sentiment held up better than expected, in large part due to another strong earnings season. Over 80% of S&P 500 companies beat consensus expectations, with notable strength in technology, industrials, and select consumer sectors. Corporate profit margins, while compressed from peak levels, remained healthy. Management teams broadly cited stable demand and productivity improvements, especially those related to automation and AI, as key performance drivers.

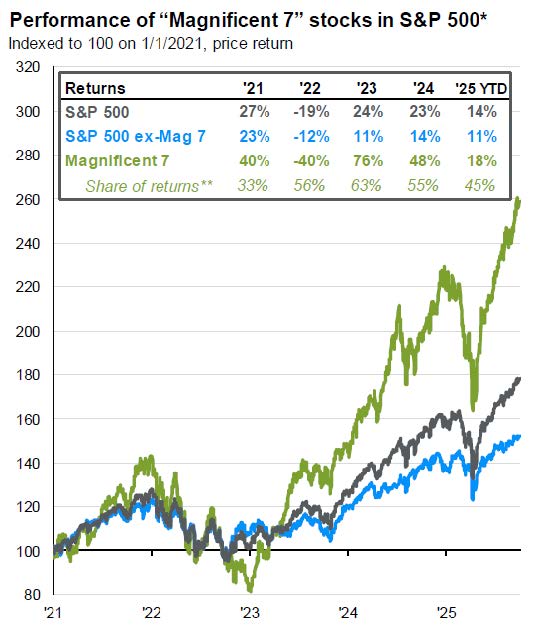

The technology sector, particularly companies tied to artificial intelligence, remained a focal point for investors this quarter. Nvidia once again posted strong results, driven by ongoing demand for AI infrastructure and semiconductors. Broader AI themes continued to benefit adjacent areas such as cloud computing, enterprise IT, and software. As monetization of AI expands beyond early adopters, these tailwinds have lifted a broad range of companies across the tech landscape. Given the varying perspectives around AI and elevated valuations in parts of the sector, we remain focused on portfolio risk mitigation through strategic position sizing, diversification, and a disciplined emphasis on high-quality companies. Our AI exposure is selective and reflects companies with established, diversified business models and longer-term secular demand drivers, rather than businesses reliant solely on AI-driven growth. While AI remains an important investment theme, it is one of many in our portfolio. We continue to pursue a range of opportunities across sectors, grounded in fundamental analysis and a balanced approach to risk and return.

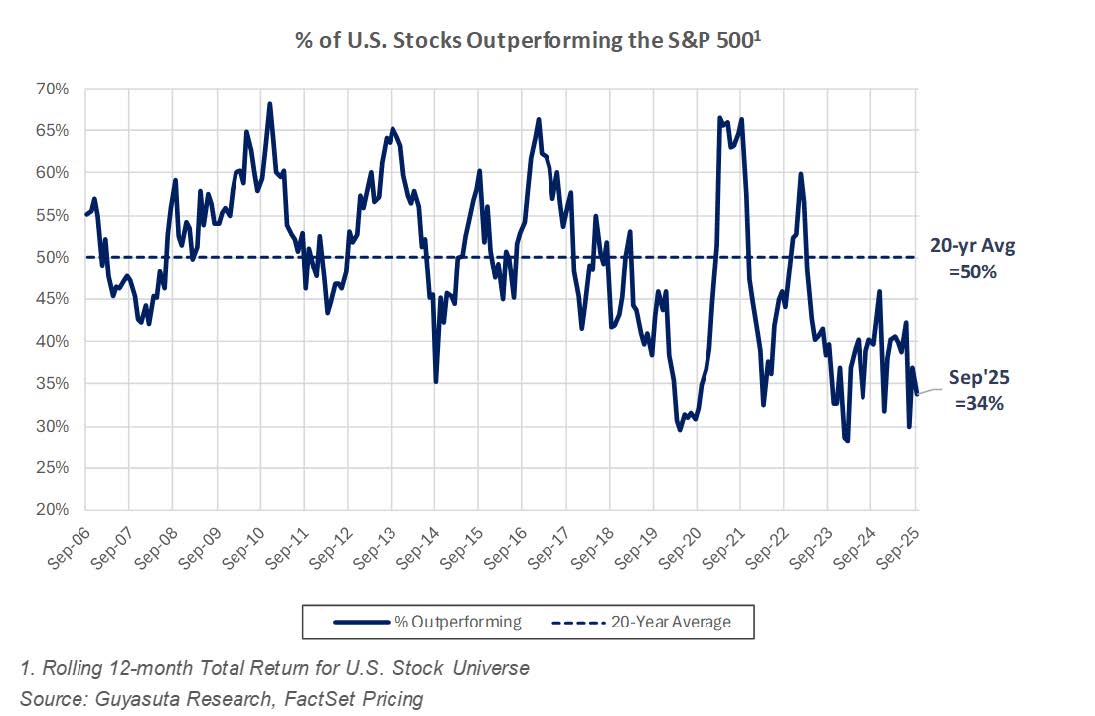

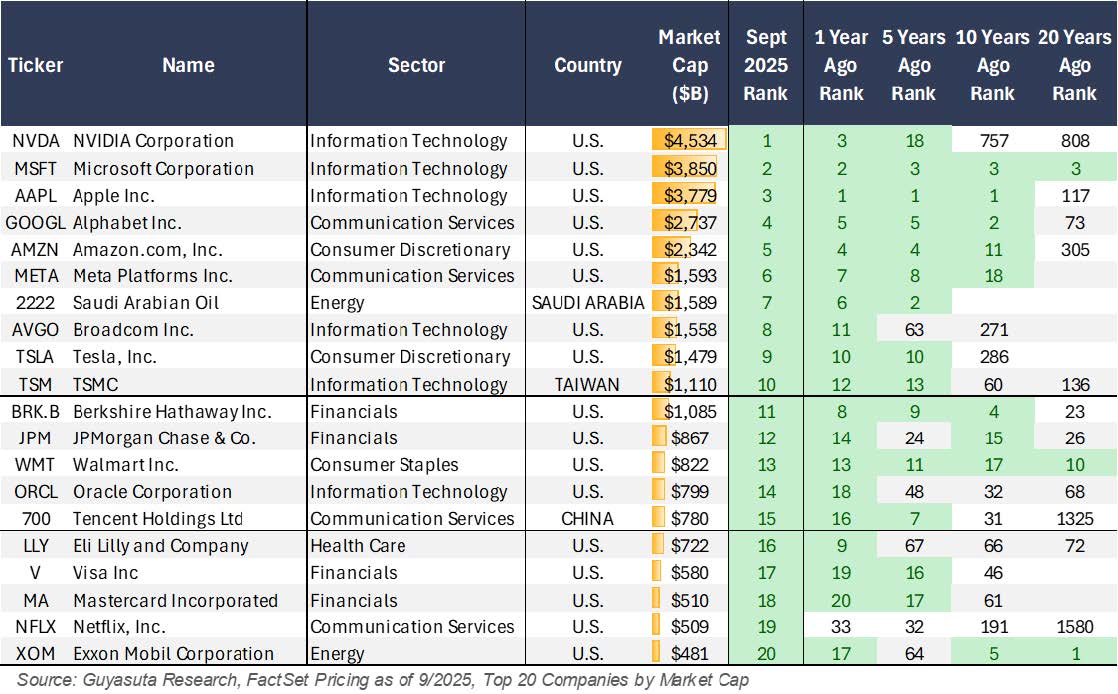

While overall equity markets have shown strength, recent performance has been led by a relatively narrow group of large-cap names. Over the past 12 months, 34% of U.S. traded stocks have outperformed the S&P 500, which is below the 20-year historical average of 50–60%. The “Magnificent Seven” continue to drive much of the gains, while small- and mid-cap stocks have generally lagged over the same period, which has presented pockets of attractive valuations and opportunity.

Looking ahead, we remain confident in our portfolio investments and approach, which focuses on high-quality, well-managed companies with durable competitive advantages and the financial strength to withstand volatility. In a market marked by ongoing innovation and shifting risks, our disciplined approach, rooted in fundamental analysis and a long-term perspective, continues to guide us. We believe this steady focus is essential to delivering consistent results for our clients over time.

Fixed Income Markets

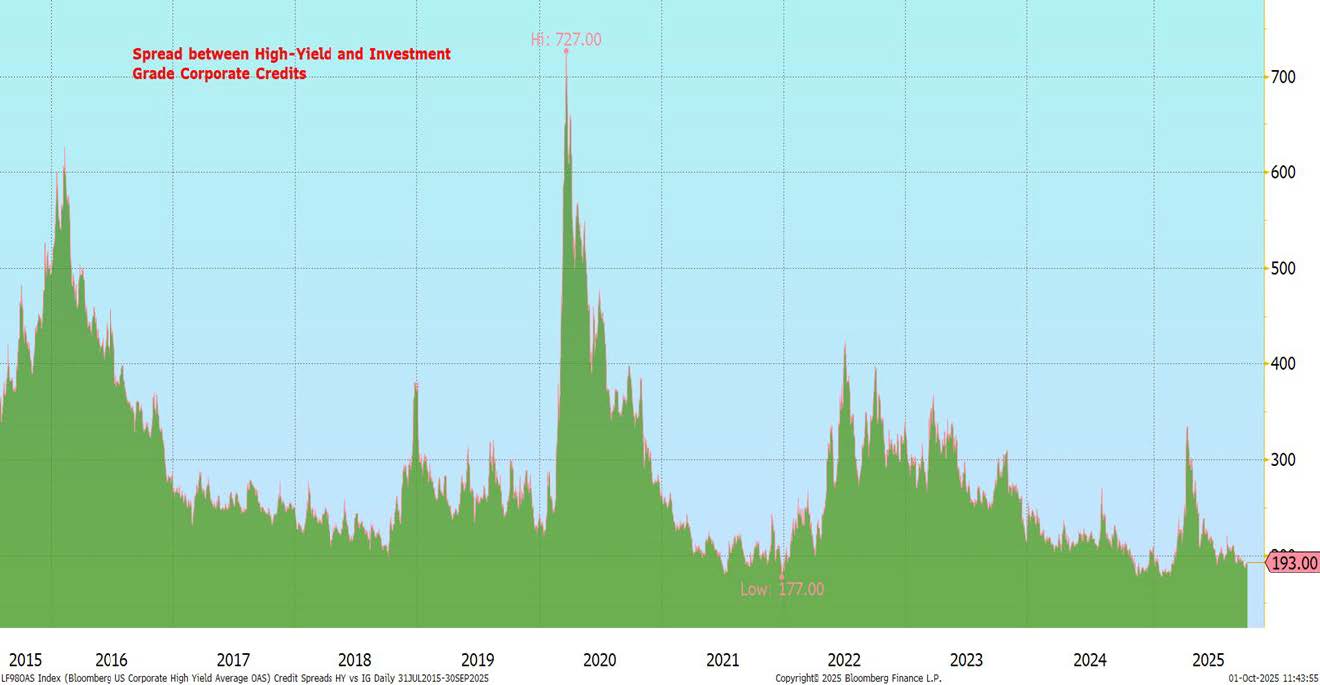

Fixed income markets responded positively to the Federal Reserve’s pivot, though persistent inflation and modest credit stress kept investors on alert. The Fed’s 25 basis point rate cut in September marked the beginning of what many expect to be a gradual easing cycle. This shift in tone supported longer-duration assets, and by quarter-end, the 10-year Treasury yield had declined modestly from 4.2% to 4.1%. Markets are now pricing in two additional cuts by year-end, which could help ease financial conditions into early 2026. This dovish turn boosted demand in high-quality fixed income. High-quality municipal bonds offered compelling tax-exempt yields across the curve. Bonds maturing in approximately twelve to fifteen years, offering nominal yields of 3.5%–4.0%, or 5.8%–6.6% on a taxable equivalent basis for high-bracket investors, were particularly attractive. Municipal credit fundamentals remain strong, making munis an attractive choice for income generation and capital preservation. Investment grade corporate bonds performed well, supported by strong balance sheets and solid earnings. Issuance remained robust, with companies taking advantage of high investor demand for bonds. Though corporate bond spreads are tight by historical standards, all-in yields remain attractive.

We are also observing early signs of strain in private credit markets, which we view as an important data point as we analyze broader credit conditions. Market data and industry reports indicate deteriorating credit quality in U.S. middle-market CLOs, rising use of payment-in-kind interest features, and weakening interest coverage ratios. Credit defaults or stress are increasingly emerging in sectors such as automotive and subprime lending, including recent auto parts bankruptcies and warning signs among subprime auto lenders. These private market signals underscore the importance of not owning low-quality credits to chase higher yields.

Though long-end rates rallied in the quarter, we continue to monitor the yield curve for signs of stress. Federal debt is now $37 trillion and the annual interest costs of servicing the debt is estimated at $952 billion per year, higher than the Department of War’s budget. Bond investors may not be rioting now, but an increase in long end rates from here would be a signal of growing unease among investors. The independence of the Federal Reserve is another risk we are monitoring. A less independent Fed not only could drive long-term rates higher but also damage confidence in the U.S. dollar and foreign investment.

Conclusion

The third quarter marked a key inflection point in monetary policy and market dynamics. A Fed rate cut, persistent inflation, strong earnings, and evolving trade tensions all contributed to a complex but ultimately resilient investment environment. While volatility and late-cycle risks remain, our focus continues to be on quality, diversification, and long-term alignment with client objectives. We thank you for your continued trust in Guyasuta Investment Advisors.

S&P 500 all-time highs

Market breadth remains narrow

Artificial intelligence stocks driving returns

S&P 500 operating margins remain high despite tariffs

Largest global companies

U.S. Core PCE remains above Fed 2% target

Corporate credit spreads are near decade lows